Netflix–Warner Bros. Discovery: A Stravus 8S operating‑model analysis

The Stravus Operating Model Series – Article 002

The issue

What the deal is

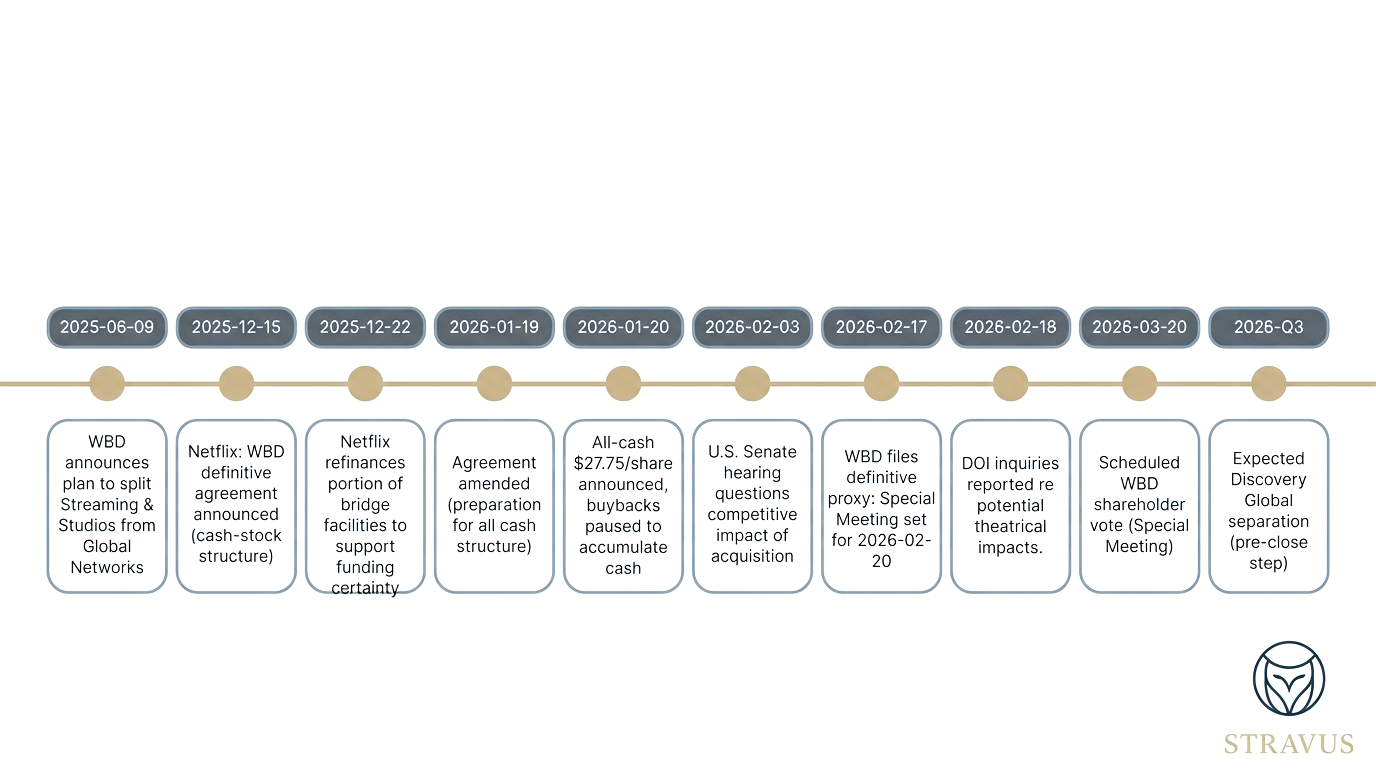

On 5 December 2025, Netflix and WBD announced a definitive agreement under which Netflix would acquire Warner Bros. (Streaming & Studios) including film and television studios, HBO Max and HBO, with Discovery Global (WBD Global Networks) spun out prior to closing.

The original structure was a cash‑and‑stock consideration (e.g., $23.25 cash + ~$4.50 Netflix stock per WBD share), valuing the transaction at $27.75 per share, implying ~$72.0bn equity and ~$82.7bn enterprise value.

On 19–20 January 2026, the parties amended the agreement to an all‑cash $27.75 per share structure.

WBD’s Special Meeting to vote on the merger is scheduled for 20 March 2026.

Market reaction and the core operating‑model question

The market has treated the deal as a material risk event for Netflix:

US$40bn of Netflix market value was wiped out “in just six sessions” amid scepticism around the acquisition (Bloomberg).

Netflix shares have “lost some 20% in value since the company launched its bid for Warner Bros in early December” (Reuters).

Reuters also reported that by mid‑January Netflix shares had fallen ~15% since announcing the merger on 5 December, citing a close around $88 and referencing the original collar floor.

The operating‑model question is therefore:

Is this acquisition a bolt‑on content/library expansion, or a redefinition of Netflix’s operating model - and is the sell‑off pricing rational execution risk, or short‑termism against a structurally coherent long‑term move?

Deal timeline

Netflix - WBD deal timeline

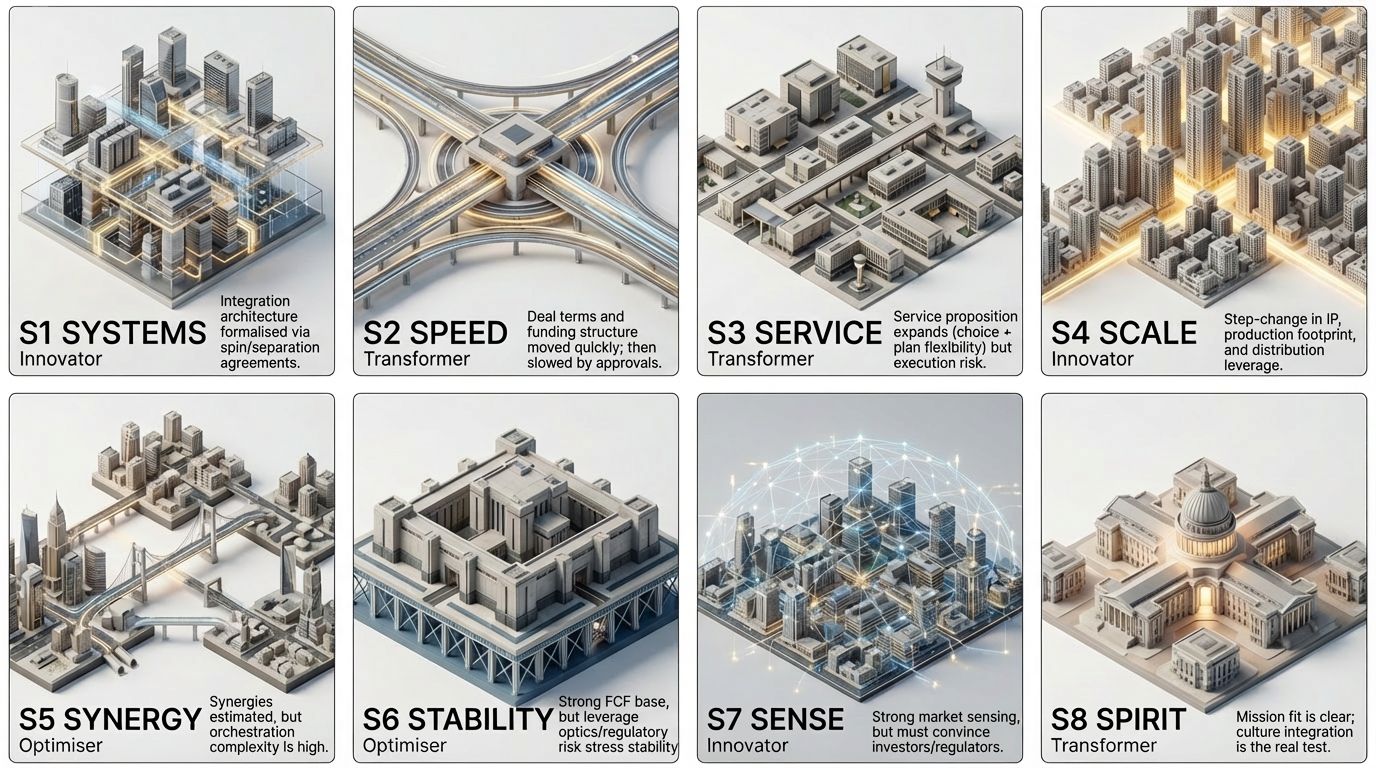

Stravus 8s Diagnostic Snapshot

Using the Stravus 8S Digital Readiness Model (as explained here), we assess Netflix’s post-acquisition operating model across eight equal dimensions of organisational maturity.

Most commentary focuses on one angle:

“It’s too much debt.”

“It’s an integration risk.”

“It’s a content land grab.”

The 8S model refuses reductionism.

Each S carries equal weight. Each one affects the others. It’s not about strength or weakness - it’s about maturity balance. Each dimension is assessed using the Stravus maturity model (as explained here).

A company can operate at Innovator-level in some areas, while lagging at Optimiser or even Survivor levels elsewhere. That imbalance is where execution risk lives - and where transformation either accelerates or fractures.

Below is a diagnostic snapshot of what this move implies for Netflix’s operating model and where the structural tension may lie.

S1 Systems - Innovator

Netflix demonstrates system‑level maturity in building and financing a complex separation‑then‑acquisition structure. The amended merger architecture includes multiple defined agreements (employee matters, IP, tax, transition services), signalling formal choreography for how operations and systems will be disentangled (Discovery Global) and then integrated (Netflix + Streaming & Studios).

The key risk is not system design; it is system integration load. The proxy/merger structure implies Netflix will run parallel operating systems (platform + studio + premium brand HBO) for a period - an Innovator challenge that must be managed without service degradation.

S2 Speed - Transformer

Speed is evident in Netflix’s rapid strategic and financial moves: after announcing the deal in early December, Netflix re‑cut the structure to all‑cash, explicitly to accelerate clarity and the path to vote, and adjusted funding commitments accordingly.

However, the operating‑model tempo then shifts into “regulated speed”: closing is expected in 12–18 months, contingent on separation completion and regulatory approvals, so execution becomes a long‑cycle program rather than a fast product iteration.

S3 Service - Transformer

Service is where Netflix argues the strongest customer logic: it expects “more choice and greater value” from combining deep libraries and HBO/HBO Max programming, and explicitly outlines more personalised and flexible subscription options once HBO Max is added.

Transformer is appropriate because the proposition is compelling, but it is not yet operationalised: migrating customers, harmonising plans, and avoiding brand dilution (especially HBO’s prestige positioning) are execution‑heavy service design problems.

S4 Scale - Innovator

The deal is structurally about scale: Netflix combines its global platform with Warner Bros.’ and HBO’s content machine, explicitly citing expanded production capacity and long‑term investment in original content.

This is an Innovator‑level move because it changes the industry’s centre of gravity: Netflix would own premier IP pipelines and global distribution, narrowing the distance between content creation and consumer demand signals.

S5 Synergy - Optimiser

Netflix forecasts meaningful value creation through integration leverage: it expects at least US$2–3bn in annual cost savings by year three, and GAAP EPS accretion by year two.

Yet synergy maturity is Optimiser because the hardest synergies here are not procurement or overhead—they are operating‑model synergies: aligning theatrical economics, premium brand management, content greenlighting, and platform distribution in one coherent cadence. Regulatory scrutiny of theatrical impacts underscores how operational choices (release windows, output levels) can become merger‑risk variables.

S6 Stability - Optimiser

Netflix enters this deal from a position of improving financial stability: for FY2025 it reported US$9.5bn free cash flow, and it forecasts ~US$11bn FCF for 2026, even while including acquisition‑related expenses in margin outlook.

But stability is stressed by financing optics and uncertainty: Netflix disclosed large bridge and term‑loan facilities tied to deal funding and increased commitments to support the all‑cash structure; it also stated it would pause buybacks to accumulate cash. Public credit and leverage commentary is mixed but informative: Moody’s affirmed Netflix’s rating (A3) while shifting outlook to stable, and Bloomberg Intelligence estimates post‑deal leverage around 3.7x EBITDA with a path down as earnings grow (Fortune).

S7 Sense - Innovator

Netflix’s “Sense” capability - market reading and decision intelligence - shows up in how it frames competition and attention share. In its Q4 materials, Netflix explicitly benchmarks its share of TV time against broader competitors and positions the deal as accelerating long‑term strategy.

However, the investor reaction signals a trust gap in the translation layer: the market is pricing not just financial leverage, but the probability of operating‑model mis‑execution. The Senate hearing and DOJ theatre inquiries illustrate that “Sense” must extend beyond consumer choice into policymaker and ecosystem assurance.

S8 Spirit - Transformer

The mission narrative is strong and coherent: Netflix’s co‑CEO explicitly anchors the deal to Netflix’s mission to “entertain the world” and frames the combination as defining “the next century of storytelling.”

Spirit is Transformer (not Innovator) because cultural integration remains the decisive variable. Netflix is moving away from a long‑standing “build” posture into a historic, identity‑defining merger; the internal cultural system must absorb major‑studio norms without losing Netflix’s agility.

Netflix - Stravus 8S operating model diagnostic summary.

Overall maturity classification

Overall profile: Late Transformer with Innovator peaks, constrained by Optimiser‑level Synergy and Stability under deal stress.

Imbalance pattern:

Innovator: Systems, Scale, Sense

Transformer: Speed, Service, Spirit

Optimiser: Synergy, Stability

Systemic opportunity: Netflix is attempting to convert its platform leadership into a fully integrated entertainment operating model - one that can arbitrage distribution, IP development, and consumer data at global scale. The press‑release commitments on cost savings and EPS accretion, plus Netflix’s strong cash generation guidance, indicate the intent to make this economically self‑funding over time.

Systemic risk: the deal concentrates execution risk in the two dimensions investors care about most during megamergers: Synergy realisation and Stability (balance sheet + regulatory clearance + ecosystem licence to operate). The documented market‑value wipeout and continued scrutiny by policymakers/theatre chains suggest Netflix must treat these as first‑class operating‑model workstreams, not post‑close clean‑up.

Stravus recommended pathway

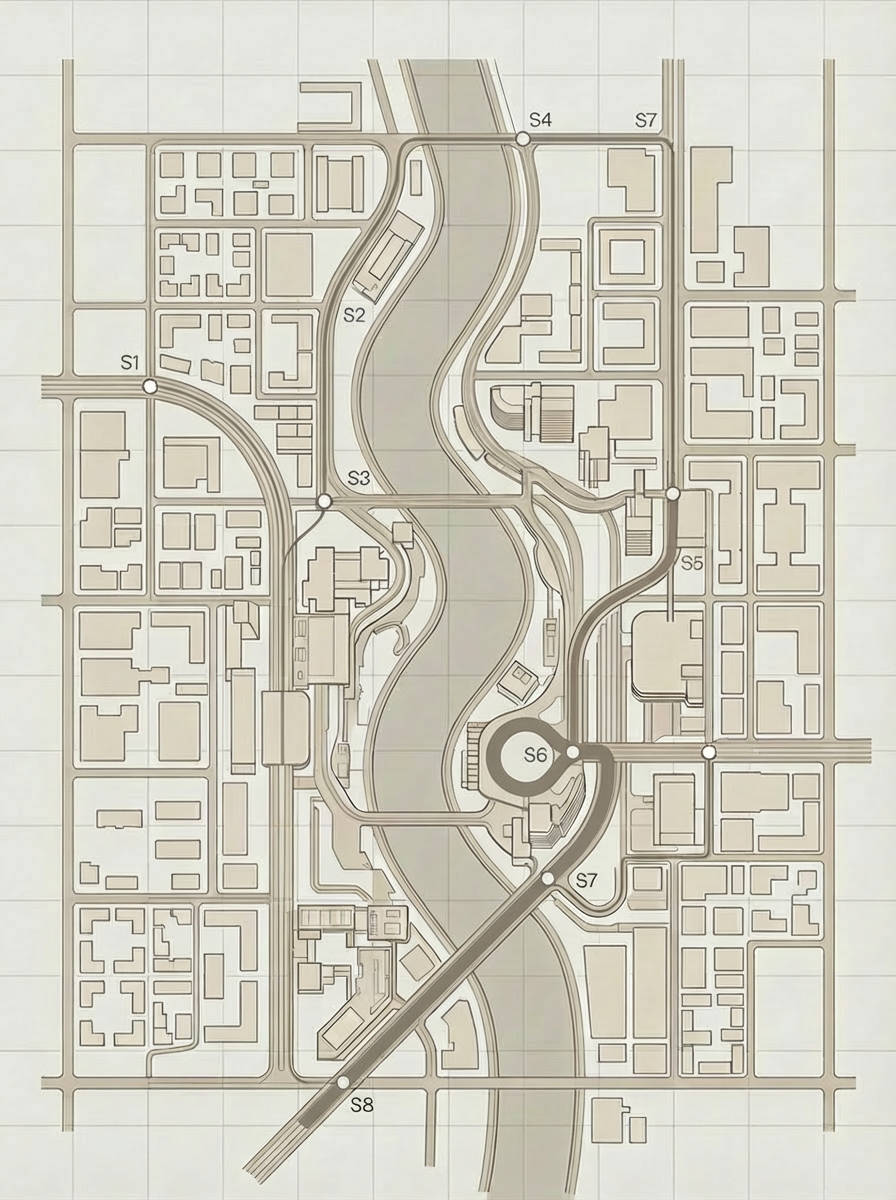

As explained in The Return of the Roaring 20s, we use the metaphor of a modern city to represent an organisation’s operating model. Each of the 8S dimensions is a critical district - interdependent, constantly in motion. Transformation is not a straight line; it requires deliberate movement across these interconnected domains.

The Stravus pathway visual uses a metro map to illustrate that journey. The route isn’t arbitrary - it reflects a sequenced, system-level redesign. Each station matters. The order matters more.

Below is Netflix’s recommended operating model synchronisation pathway, following its acquisition of Warner Bros Discovery and is explained below the image. This pathway is sequenced to synchronise maturity - specifically pulling Synergy and Stability up to match the Innovator‑level ambition embedded in Systems/Scale/Sense.

Netflix - WBD pathway.

Quick wins

Stability assurance pack (capital + clarity).

Codify, in public terms, a de‑leveraging and liquidity policy that ties directly to the company’s own disclosed cash‑flow guidance: FY2025 US$9.5bn FCF, FY2026 forecast ~US$11bn, and the stated intention to pause buybacks to build cash for the transaction. This is about translating “we can fund this” into an explicit rule set (liquidity floor, leverage ceiling, buyback re‑start triggers).

Synergy blueprint before Day 1.

Turn the headline US$2–3bn cost‑savings by year three into a transparent operating‑model map: which synergies are platform/tech, which are marketing, which are overhead, and which are content pipeline/rights economics. Investors discount vague synergy statements; they re‑rate specific synergy mechanics.

Ecosystem licence to operate (theatrical + creators).

Given DOJ interest in potential theatrical impacts, operational commitments (release windows, slate discipline, and cinema economics) should be formalised as policy—because regulators and theatre chains will treat them as merger‑relevant “systems,” not PR.

Medium‑term moves

Architect a dual‑brand service strategy, not “everything becomes Netflix.”

Service maturity depends on whether Netflix can integrate HBO/HBO Max value without diluting HBO’s premium identity. The operating model should explicitly define where HBO remains distinct (content standards, brand rules) versus where the platform converges (identity, billing, recommendation, plan bundles). Netflix’s stated goal of more personalised/flexible plans becomes the execution design brief.

Build a “Studio Operating System” layer.

Netflix’s core systems are optimised for streaming distribution. Owning a major studio requires production governance, slate risk management, and long‑horizon portfolio economics—capabilities implied by the commitment to maintain Warner operations and expand production capacity. A dedicated studio OS is how you prevent cultural and operating frictions from becoming instability shocks.

Synchronise decision cadence between platform and studio.

The new operating model must resolve a central tension: platforms iterate quickly; studios plan in multi‑year cycles. Treating this as a synergy problem (Optimiser) rather than a systems problem (Innovator) is where integrations fail. The mechanism is a unified greenlight council with explicit decision rights, capital allocation rules, and a feedback loop from distribution data to development choices. (This is inference, grounded in the structural shift described in filings and the stated intent to maintain operations.)

Investor‑focused verdict: justified or short‑sighted?

What the sell‑off is correctly pricing:

The deal is a step‑change in complexity and leverage optics; Netflix itself disclosed large bridge/term‑loan facilities and paused buybacks to accumulate cash, and the market erased ~US$40bn of value quickly amid scepticism.

Regulatory scrutiny is real: Senate questioning and reported DOJ outreach to theatre chains indicate that clearance and behavioural commitments may be harder than a conventional tech M&A process.

What the sell‑off may be under‑weighting:

Netflix’s cash‑generation base (US$9.5bn FCF FY2025; ~US$11bn forecast FY2026) and stated intent to preserve investment‑grade posture suggest capacity to “grow into” the deal if execution is disciplined.

Public credit analysis (Moody’s affirmation; Bloomberg Intelligence leverage path) implies the transaction can be de‑levered if earnings perform and integration does not destroy operating momentum.

Bottom line: the 8S view suggests the sell‑off is not irrational - it reflects real Synergy and Stability execution risk. But it could prove short‑sighted if Netflix executes the maturity‑synchronisation pathway: (1) formalise stability rules, (2) operationalise synergy mechanics, (3) harden ecosystem commitments, and (4) design a dual‑cadence platform‑studio operating system. The market’s judgement will hinge less on the headline deal price and more on whether Netflix can eliminate the operating‑model imbalance highlighted by this diagnostic.

Illustrative free cash flow and leverage comparison

All figures on the right are publicly stated or publicly estimated and should be treated as illustrative (final financing and pro forma outcomes will depend on close timing, interest rates, and integration performance).

Prioritised sources

Primary / official filings and releases

Netflix & WBD transaction announcement (Netflix IR, 5 Dec 2025).

Netflix Q4 FY2025 results and forecast (SEC exhibit / shareholder letter extract, includes FCF, debt, bridge facilities).

Netflix 8‑K describing amended merger agreement mechanics (including Discovery Global net‑debt “Specified Amount” and net‑debt adjustment).

WBD definitive proxy statement and Special Meeting details (DEFM14A, 17 Feb 2026).

Major financial press

Reuters coverage of deal terms, break fees, synergy expectations, vote timing, and regulatory scrutiny.

Financial Times reporting on the renewed bidding context and upcoming shareholder vote (accessible abstract).

Credible industry / credit analysis

Bloomberg on market‑cap impact around announcement window.

Fortune (credit/leverage estimates; Moody’s rating commentary).

Morningstar industry valuation/regulatory perspective.