Hims & Hers: A Stravus 8S Operating Model Analysis

The Stravus Operating Model Series – Article 003

The issue

What the deal is

Hims & Hers’ agreement to acquire Eucalyptus is structured as follows (publicly disclosed in an SEC 8‑K and the company announcement):

Enterprise value / consideration: up to ~US$1.15b.

Funding and form: ~US$240m cash payable at close; ~US$710m deferred over 18 months; up to ~US$200m earn‑out tied to revenue and adjusted EBITDA targets through fiscal years 2026–2028 (payable after annual results).

Settlement flexibility: Hims may (for specified sellers) settle up to ~60% of deferred and earn‑out obligations in Class A shares; it states it is prepared to finance most of the transaction with cash on hand and future operating cash flows.

Timing and conditions: expected to close mid‑calendar 2026 / mid‑fiscal 2026, subject to customary conditions and “required regulatory approvals”; the deal is governed by New South Wales law.

People / continuity: Eucalyptus CEO Tim Doyle is expected to become SVP International at Hims, overseeing its international business.

Strategic intent is explicit: Hims says Eucalyptus’ footprint enables entry into Australia and Japan and deepening in the UK, Germany, and Canada; it emphasises local regulatory expertise and a “diversified international platform” spanning online pharmacy fulfilment through concierge‑style service. Eucalyptus is described as Australia’s largest digital health provider, having facilitated nearly two million consultations and being the first Australian telehealth company accredited by the Australian Council on Healthcare Standardsagainst EQuIP6 standards.

Market reaction, in context of the FDA overhang

On the day of announcement (19 February 2026), Reuters reported Hims & Hers shares rose ~7% in pre‑market trading. But that pop sits inside a much larger downtrend driven by regulatory risk: Reuters reported the stock was off more than 45% since the early‑February pill announcement fiasco. Independent market‑data sources show HIMS closing at ~US$15.82 on 19 February, after falling sharply from late‑January levels and experiencing extreme volatility through the week of the FDA actions and litigation.

This isn’t new. In its 2024 annual report, Hims disclosed it began offering compounded injectable semaglutide in May 2024 and explicitly warned that compounding permissions depend on shortages and narrow exemptions under sections 503A/503B of the FDCA; it also flagged that enforcement actions could include warning letters, injunctions, seizures and fines. Those risks materialised in February 2026 when the FDA publicly warned it would take “decisive steps” against mass‑marketed non‑approved compounded GLP‑1 products (naming Hims) and noted potential legal action for violations.

The central operating‑model question

Bolt‑on thesis: Eucalyptus is a geographic bolt‑on that adds customers (~775,000), brands (including Juniper and Pilot), ARR run‑rate (>US$450m), and local operational capability, while Hims keeps its core U.S. operating model largely intact.

Redefinition thesis: This acquisition forces a re‑architecture of operating model fundamentals - multi‑jurisdiction regulatory compliance, clinical governance, data protection, and cross‑market brand/platform integration. Hims’ own filings already emphasise that international jurisdictions impose varying requirements around telehealth, advertising of prescription products, compounding, and data protection - i.e., the operating model cannot simply be “copied and pasted.”

Given the regulatory shock in the U.S. (and the market’s repricing of HIMS accordingly), the deal’s strategic sense hinges on whether Eucalyptus reduces the firm’s regulatory concentration risk - or unintentionally amplifies it. Australian reporting has argued Eucalyptus has increasingly concentrated on weight loss/GLP‑1, which would make this less of a diversification play and more of a global scaling bet on the GLP‑1‑enabled consumer health category.

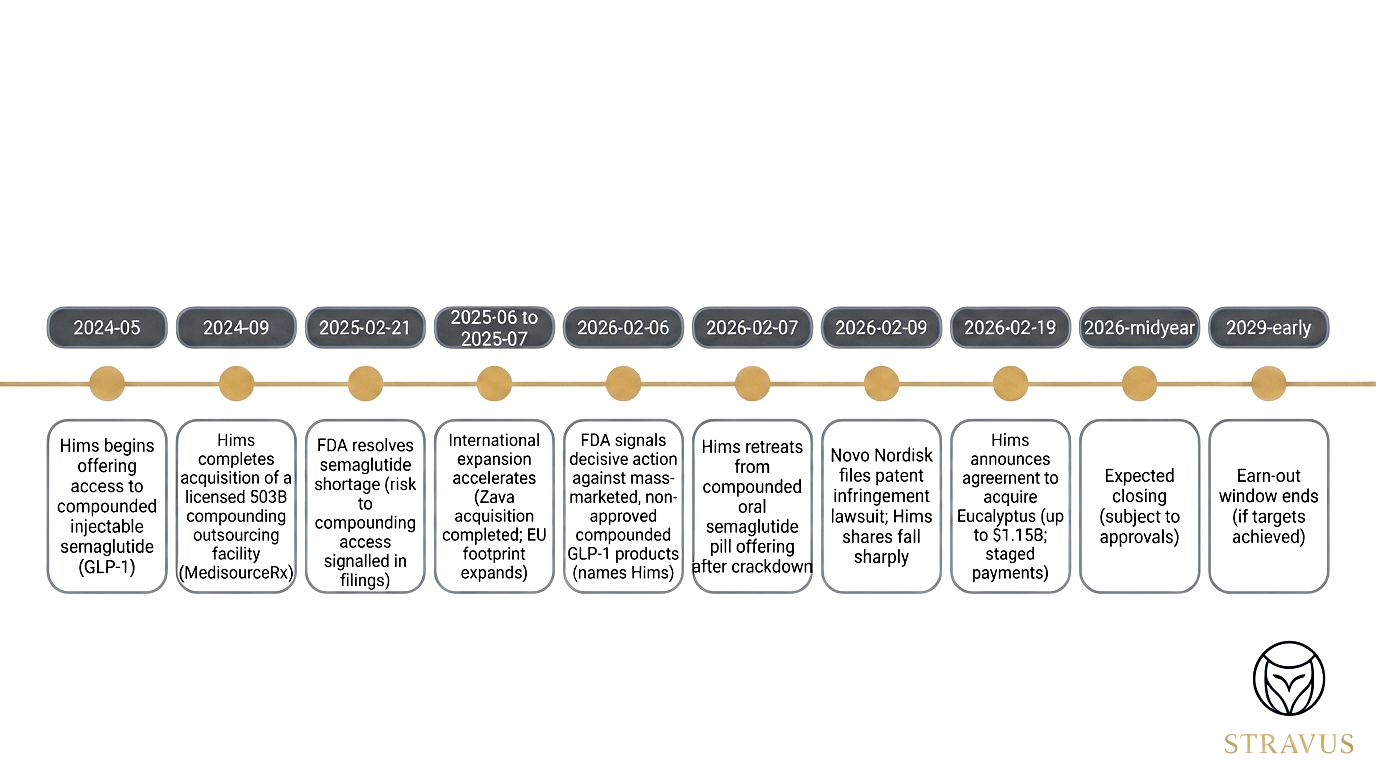

Deal timeline

HIMS timeline.

Assumptions and data cut‑off

Data cut‑off is 20 February 2026 (Australia/Sydney). This diagnostic uses public information only (press releases, filings, credible press); it does not include internal operating metrics, confidential integration plans, or non‑public regulatory correspondence.

Stravus 8s Diagnostic Snapshot

Using the Stravus 8S Digital Readiness Model (as explained here), we assess Hims’ post-acquisition operating model across eight equal dimensions of organisational maturity. This snapshot assesses public signals only (official filings, announcements, credible press) and should be read as a structural diagnosis - not a moral judgement.

Most commentary isolates one theme:

“It’s a distraction from FDA pressure.”

“It’s a global land grab.”

“It’s a burn on short-term cash.”

The 8S model refuses that kind of reductionism. Each S carries equal weight. Each one affects the others. It’s not about strength or ambition - it’s about maturity alignment. Each dimension is assessed using the Stravus maturity model (as explained here).

A company can operate at Innovator level in some domains and still be under strain due to unresolved gaps elsewhere. That’s where friction accumulates. And where even promising strategy can destabilise execution.

Below is the diagnostic snapshot: what the public signals suggest about Hims’ current structure and whether this deal adds resilience or intensifies imbalance.

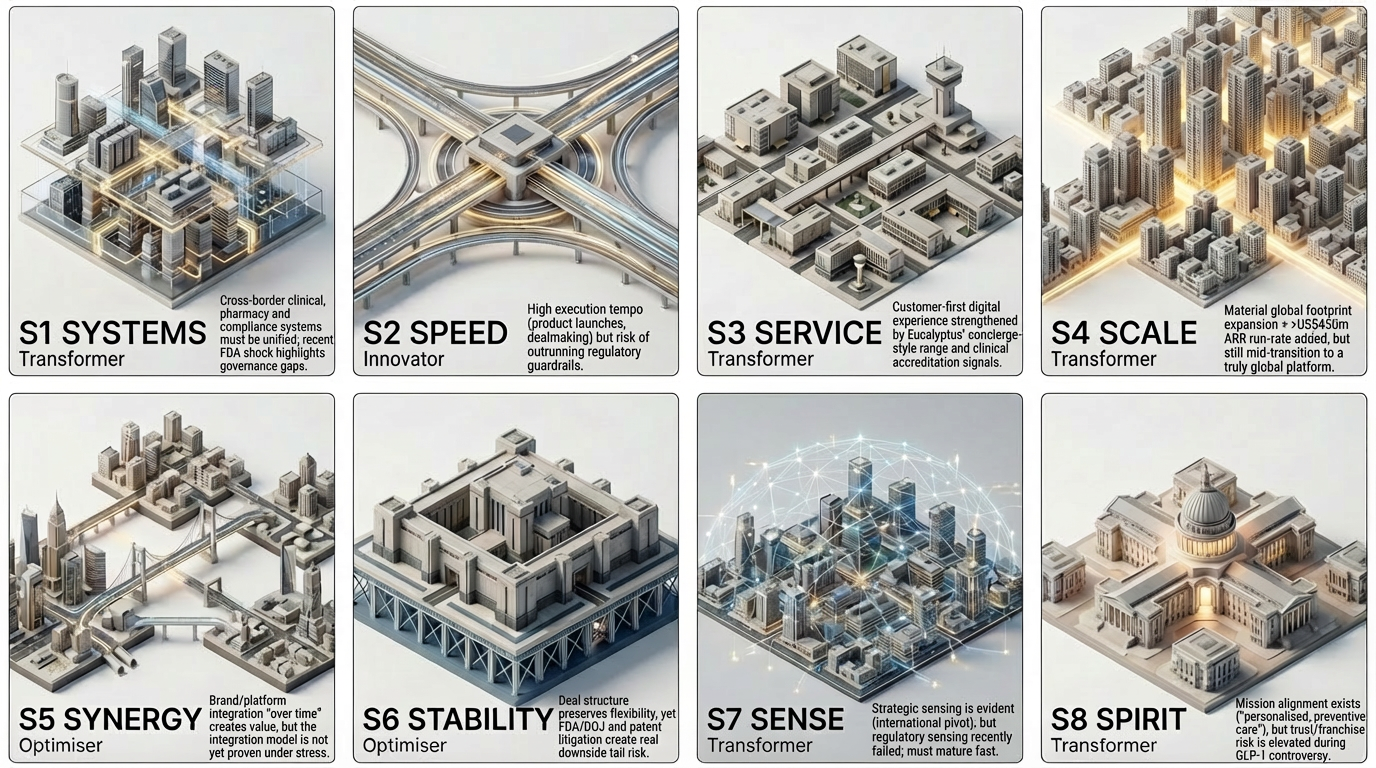

S1 Systems - Transformer

Hims is intentionally building a platform that spans telehealth, fulfilment and (via 503B/503A pathways) compounding access; its filings show how tightly its product economics and growth have been coupled to complex regulatory exemptions. The acquisition adds multi‑country operations and requires repeatable, auditable systems for prescribing, pharmacy fulfilment, clinical governance, and marketing compliance across jurisdictions—an operating‑model step‑change rather than a plug‑in.

S2 Speed - Innovator

Speed is both capability and liability here. Hims has demonstrated rapid expansion through multiple acquisitions (e.g., Zava in Europe; Livewell in Canada) and fast product iteration. The February 2026 GLP‑1 pill episode shows the same speed can outrun regulatory certainty - forcing retreats within days and triggering enforcement escalation.

S3 Service - Transformer

Service maturity is strengthened by combining two consumer‑led care models. Hims positions itself as “customer‑first” and personalised; Eucalyptus is described similarly, with clinical rigour and a simple digital experience, plus publication of peer‑reviewed outcome research and ACHS accreditation in Australia - important trust signals in healthcare. The service upside is not only breadth (more programs, more markets) but depth: the deal narrative explicitly spans pharmacy fulfilment through concierge‑style service.

S4 Scale - Transformer

Scale is the clearest strategic motive. Eucalyptus adds a >US$450m annual revenue run‑rate and ~775,000 customers, and materially expands Hims’ international addressability (Australia/Japan entry; deeper UK/Germany/Canada). However, “global platform” scale is constrained by regulation and localisation needs; Hims’ filings explicitly note that international expansion imposes varying requirements around telehealth, advertising, compounding and data protection—scale must be built with compliance architecture, not against it.

S5 Synergy - Optimiser

Hims states Eucalyptus’ brand portfolio will “transition into Hims & Hers over time,” implying purposeful integration rather than immediate consolidation. But the hard part is Synergy design: what stays local versus central, how clinical governance is standardised, and whether international growth is a federation of local operators or a single global operating system.

This is where the Australian context matters: reporting suggests Eucalyptus has become increasingly weight‑loss/GLP‑1 centric. If true, synergy is not “diversification away from GLP‑1 risk,” but “scale GLP‑1‑adjacent consumer care globally”—which increases the premium on integration discipline and regulatory foresight.

S6 Stability - Optimiser

Management is clearly trying to protect Stability: only ~US$240m is due at closing; much of the remainder is deferred/earn‑out, and Hims can settle some amounts in stock (subject to limits and seller eligibility). This is a Stability‑preserving deal design given the company’s recent volatility.

But Stability is still under strain because regulatory and legal headwinds are active, not hypothetical. The FDA explicitly named Hims in its February 2026 enforcement statement on non‑approved compounded GLP‑1s, and Reuters reported potential DOJ follow‑through (injunctions/fines) remains possible despite the product retreat. At the same time, Hims’ market cap has sharply compressed and shares have traded at a fraction of prior highs - raising the cost of equity if the company needs additional funding flexibility.

S7 Sense - Transformer

The acquisition reflects strategic sensing: Hims is attempting to reduce geographic concentration and strengthen its appeal as a scaled distribution partner for treatments and diagnostics. Yet the GLP‑1 pill episode exposed a gap in regulatory sensing - the ability to anticipate enforcement posture, not just consumer demand. Sense is therefore mid‑high maturity, but not at “always‑on, ahead‑of‑regulator” level.

S8 Spirit - Transformer

Spirit is mission and trust. Both companies frame the combined vision around accessible, personalised care, with Eucalyptus explicitly speaking to prevention rather than “merely treating disease.” The challenge is that the public narrative around compounded GLP‑1s can collide with healthcare trust—especially when regulators describe products as illegal “copycats” and threaten enforcement tools.

HIMS - Stravus 8S snapshot

Overall maturity classification

Overall profile: High Transformer with a pronounced imbalance (Speed/Scale/Service outpacing Stability/Synergy).

The systemic pattern is familiar: the organisation can move fast and scale geographically, but healthcare platforms accumulate structural stress when compliance, clinical governance, and cross‑market integration discipline lag momentum. Hims’ own prior filings explicitly warn that compounding permissions and advertising constraints are narrow, and that failure to meet exemption conditions can trigger enforcement actions. The recent FDA/DOJ escalation shows that stress is now active.

The opportunity is equally clear: if Hims uses Eucalyptus to upgrade the operating model(not just expand footprint), it can convert international expansion into a stabilising hedge. If it treats the acquisition as purely additive scale while the U.S. regulatory issue remains unresolved, execution risk compounds.

Stravus recommended pathway

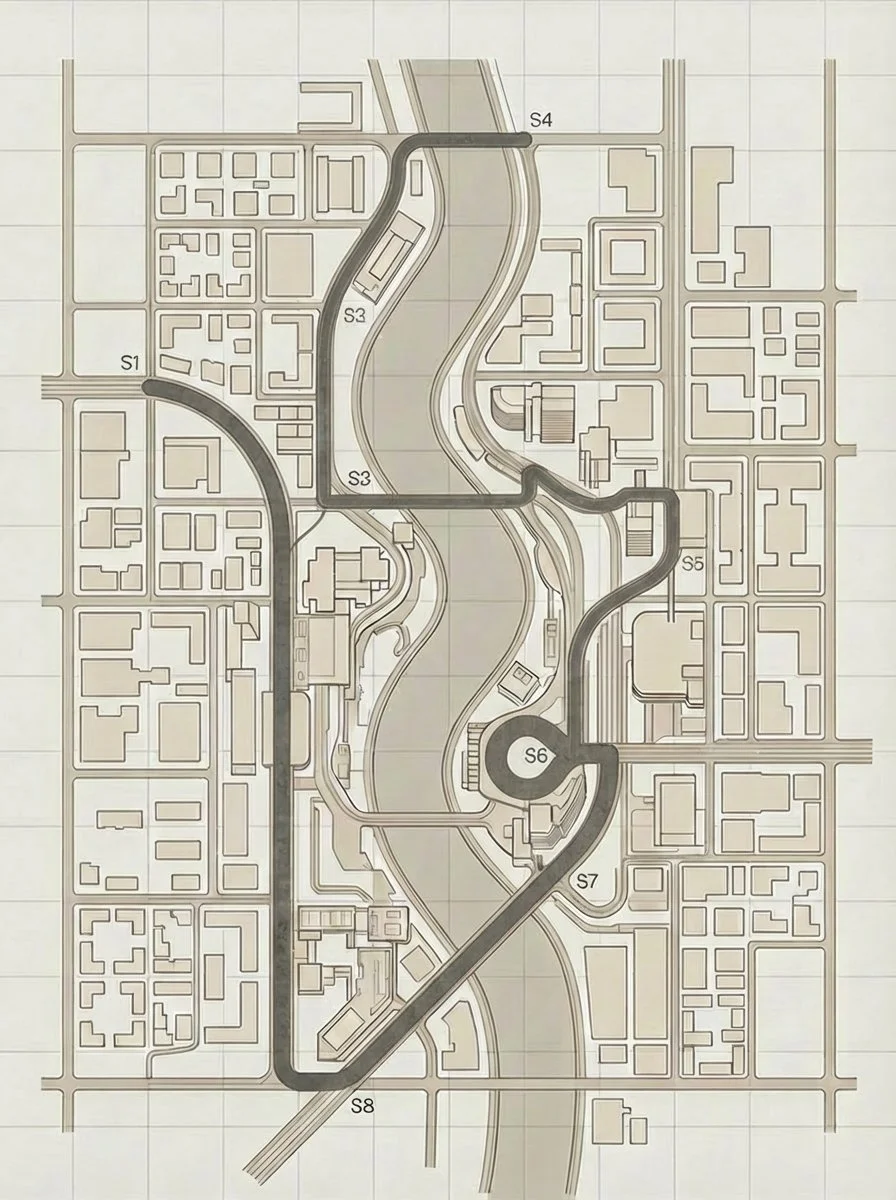

As explained in The Return of the Roaring 20s, we use the metaphor of a modern city to represent an organisation’s operating model. Each of the 8S dimensions is a critical district - interdependent, constantly in motion. Transformation is not a straight line; it requires deliberate movement across these interconnected domains.

The Stravus pathway visual uses a metro map to illustrate that journey. The route isn’t arbitrary - it reflects a sequenced, system-level redesign. Each station matters. The order matters more.

Below is Hims’ recommended operating model synchronisation pathway, following its acquisition of Eucalyptic and is explained below the image.

HIMS pathway.

Immediate moves

The first priority is Stability and Systems hardening—because it protects both the base business and the acquisition thesis.

Hims should treat the February 2026 enforcement episode as a trigger to implement an operating‑model “regulatory control plane”: clear global marketing standards for prescription products (especially compounded therapies), auditable personalisation criteria, and quality reporting discipline aligned to the FDA’s stated enforcement posture. The goal is not defensiveness; it is predictable execution under scrutiny.

In parallel, management should disclose (as far as public communications allow) how it will ring‑fence integration from litigation and enforcement disruption—because investors are currently pricing the risk that revenue streams connected to “grey‑zone” regulatory interpretations are conditional.

Medium‑term moves

The second priority is Synergy architecture: decide whether the international business becomes a federated model (local operators with local licences and governance) or a unified global platform. Hims’ filings show international jurisdictions impose varying requirements for telehealth, compounding, advertising and data protection; therefore, synergy must be built as standardised principles + local execution, not centralised uniformity.

A practical integration design would:

preserve Eucalyptus’ local clinical governance where it is strongest (e.g., accreditation‑driven safety processes), while aligning platform data, customer experience, and measurement;

define a single global “clinical evidence and outcomes” layer to defend trust across markets (leveraging Eucalyptus’ peer‑reviewed publications and consultation scale as credibility assets);

standardise data governance and privacy controls across all markets, anticipating the compliance costs and liabilities described in filings (a non‑negotiable operating capability in healthcare).

Scaling moves

Only after Stability + Systems are demonstrably strengthened should Hims push harder on the Scale thesis: staged entry into Australia and Japan, and deeper penetration in UK/Germany/Canada, using Eucalyptus’ local expertise as the “landing gear.” This sequencing matters because multi‑market expansion can quickly turn into multi‑market compliance exposure if growth is allowed to lead governance.

Investor‑focused verdict: justified or short‑sighted?

The market’s initial positive reaction to the acquisition (pre‑market rise) is understandable: the deal creates a credible international platform story and brings scale, customers, and local regulatory capability at a moment when U.S. regulatory concentration risk is painfully visible.

However, the broader sell‑off and compressed valuation look less like “acquisition scepticism” and more like a repricing of Stability: the FDA’s explicit enforcement posture (naming Hims), the possibility of DOJ action, and the ongoing patent dispute have shifted the risk profile. The 8S view suggests the acquisition can be strategically sound, but only if it is used to raise operating‑model maturity (Systems, Stability, Synergy) to match Hims’ Speed. Absent that, it risks becoming “more surface area” while the core regulatory stress remains.

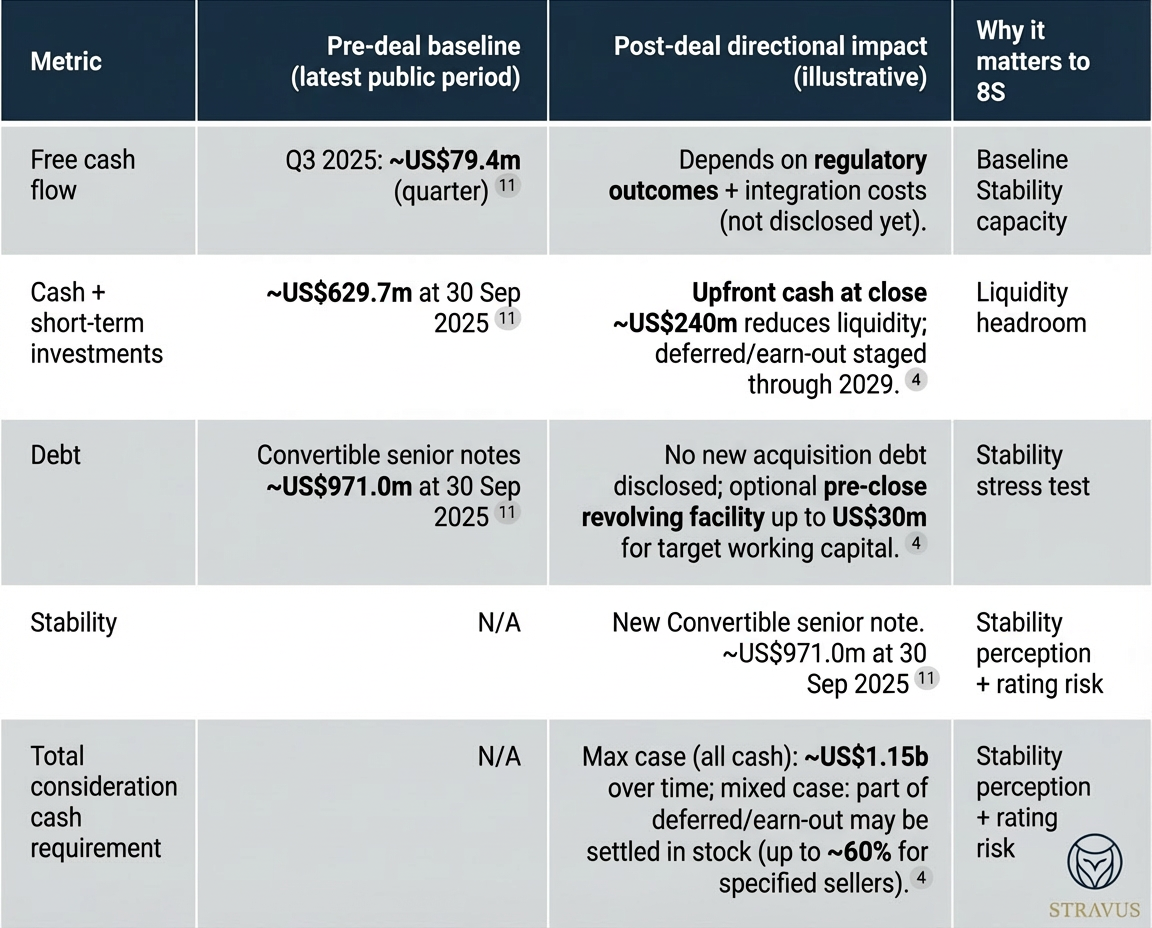

Illustrative free cash flow and leverage comparison

Data cut‑off is 20 February 2026 (Australia/Sydney). This diagnostic uses public information only (press releases, filings, credible press); it does not include internal operating metrics, confidential integration plans, or non‑public regulatory correspondence.

Prioritised sources

Primary / official

Hims & Hers press release announcing the acquisition structure, funding intent, markets, customers and ARR run‑rate.

Hims & Hers Form 8‑K detailing the Securities Sale Deed terms (deferred schedule, earn‑out mechanics, stock settlement option, closing conditions).

Hims & Hers annual report disclosures on compounding/GLP‑1 regulatory dependence and enforcement risks.

FDA press announcement on enforcement intent against non‑approved compounded GLP‑1 drugs (explicitly naming Hims).

Major press / credible industry

Reuters coverage of the acquisition and analyst framing (fit, but GLP‑1 path remains dominant theme).

Reuters coverage on DOJ referral risk and potential enforcement actions post‑retreat.

Reuters coverage on Novo Nordisk’s lawsuit and the stock reaction.

Capital Brief (Australia) on deal context and Eucalyptus’ strategic pivot toward weight loss (relevant to synergy and concentration risk).

Hims filings on international regulatory complexity across markets (telehealth, advertising, compounding, data protection).

ACCC guidance on Australia’s new mandatory merger control regime (relevant to “required regulatory approvals” for deals connected with Australia).