JOLT: A Stravus 8S Operating Model Analysis

The Stravus Operating Model Series – Article 004

Using the Stravus 8S Digital Readiness Model (as explained here), we assess JOLT’s operating model across eight equal dimensions of organisational maturity. This snapshot assesses public signals only (official filings, announcements, credible press) and should be read as a structural diagnosis - not a moral judgement.

Executive summary

JOLT’s operating model is structurally unusual (and strategically interesting): it combines urban EV charging with digital‑out‑of‑home (DOOH) media so that advertising revenue helps subsidise the driver proposition. In Australia, it positions the core consumer offer as “7kWh free every day” (service fee applies), with charging powered by 100% Aussie‑certified GreenPower.

In 2024–2025, JOLT publicly moved from “network + media inventory” toward AI‑enabled optimisation and data products. It launched Spark Intelligence to enable impression‑based planning/trading with real‑time analytics and attribution, using third‑party audience analytics (modelled from 18 million users) combined with JOLT’s first‑party data. It then added AI‑powered real‑time optimisation “at scale” with “always‑on learning”, positioning Spark as a continuously improving decision loop for advertisers. Separately, JOLT introduced AutoCharge for paid members to reduce customer friction (“plug and go”), with stated rollout to other markets.

At the same time, JOLT has announced a major scale step: a signed agreement to acquire a substantial portion of Volta Media Network from Shell, formally entering the United States. JOLT states the deal adds thousands of locations, across up to 34 states and 64 DMAs, and is expected to close 1 January 2026 (subject to conditions).

The central operating‑model question is therefore not “is AI first an optimisation or redesign? - it’s more specific:

Can JOLT simultaneously

(a) accelerate AI‑enabled optimisation (high‑tempo software/data decision loops), and

(b) integrate and scale a major U.S. footprint (site hosts, field ops, different stacks),

without Stability becoming the constraint?

Public evidence suggests JOLT is High Transformer overall, with Innovator peaks in Sense and Scale, but Optimiser‑level Stability risk - especially because EV charging reliability is judged by “successful charging”, not “uptime”.

JOLT’s Business Model

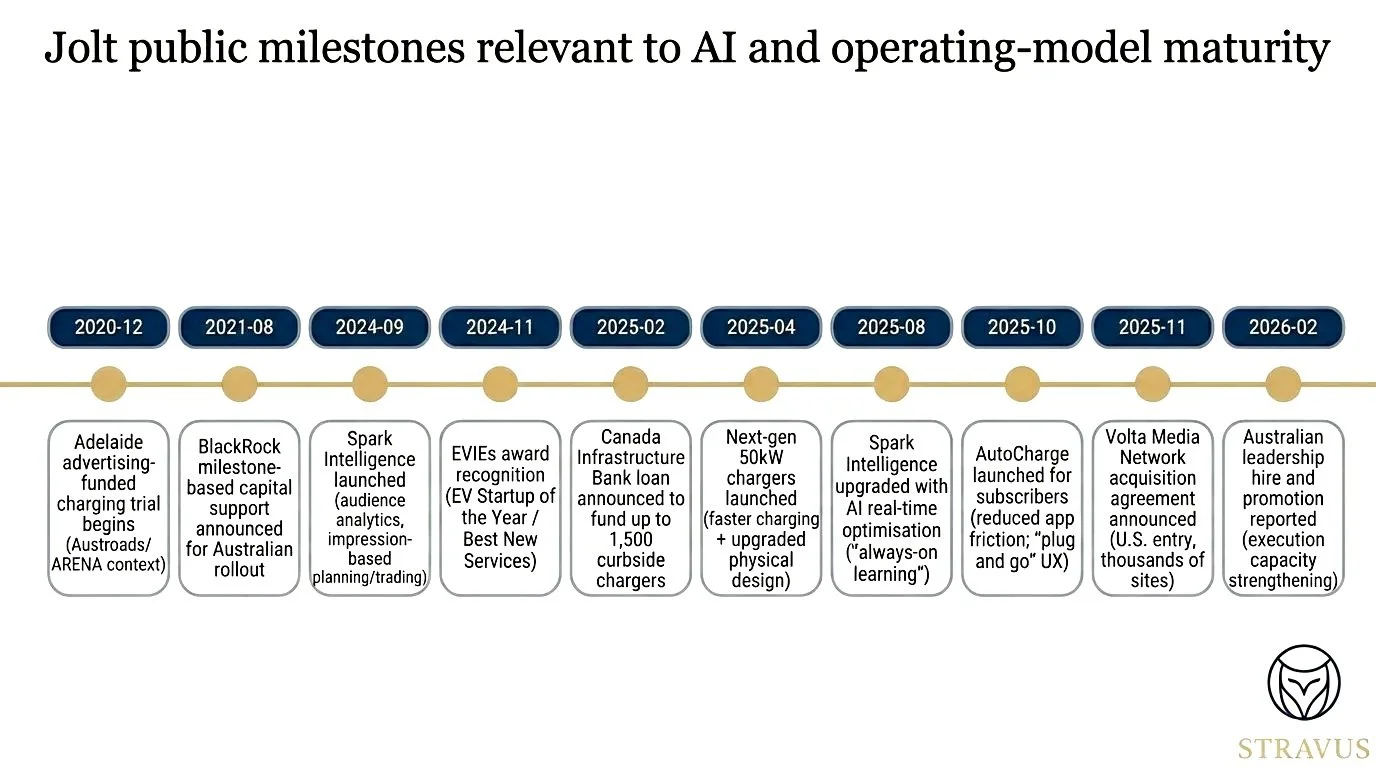

JOLT’s model can be traced in Australian public‑sector documentation. Austroads describes an advertising‑revenue‑funded metropolitan trial (Adelaide): 21 EV charging and advertising panels deployed to test whether advertising can cover both infrastructure costs and provision of free charging. Australian Renewable Energy Agency similarly announced funding for the Adelaide trial: 21 units, ~15 minutes free charging (~45 km), 100% renewable energy, and a commercial‑viability experiment for ad‑funded charging.

The strength of this model is that it creates a self‑reinforcing flywheel: more charging utilisation → more engaged audience time → stronger media proposition → more subsidy capacity → more charging adoption. JOLT’s own positioning reinforces this integrated logic (charging + digital screens + app experience).

Public signals also show JOLT has been building the infrastructure “permission stack” required for city‑embedded rollout (utilities, councils, government programs). For example, Endeavour Energy announced a partnership with JOLT to install EV chargers on existing streetside substations in Western Sydney (with a stated target of 230 stations by 2025 and 1,000+ over the next decade), and explicitly notes the 7kWh free daily concept and GreenPower sourcing.

On the capital/credibility front, BlackRock Real Assets took an equity stake and (per industry reporting) committed $100m+ through milestones to fund infrastructure build‑out (including a stated ambition of 5,000+ stations). These institutional signals matter: AI acceleration and U.S. expansion both amplify execution risk; credible funding and counterparties help, but do not substitute for operating maturity.

Market and reputation signals

Because Jolt is private, the most credible “market” signals are reputation, awards, and counterparties:

Jolt reports it was named EV Startup of the Year (and Best New Services) at the Electric Vehicle Innovation & Excellence Awards (EVIEs).

Jolt and trade coverage reference recognition via TIME and Statista rankings of top greentech companies, supporting brand legitimacy for councils/partners and advertisers.

Public‑sector programs (ARENA trial; council approvals; Transport for NSW references to Jolt in its EV charging program documents) show the model has been accepted within civic infrastructure constraints.

Public signals of a transition to AI‑enabled product and optimisation

JOLT’s transition to AI‑enabled optimisation is explicit in its own announcements:

Spark Intelligence (September 2024): positioned as an “industry‑first” platform to revolutionise planning/trading/reporting for out‑of‑home, enabling impression‑based approaches, real‑time analytics, attribution/measurement, and blending audience analytics (modelled from 18 million users) with geo‑spatial planning and measurement tools.

AI real‑time optimisation (August 2025): a “significant enhancement” enabling advertisers to use AI to optimise campaigns in real time, at scale, using in‑flight performance tracking and “always‑on learning.”

AutoCharge (October 2025): plug‑and‑go functionality for JOLT Plus members; JOLT describes secure recognition and instant session start, with rollout to other markets.

In other words, JOLT is not merely operating chargers: it is building a decision system (Sense) and a software‑mediated service layer (Service).

U.S. expansion via Volta and why it changes the operating challenge

Jolt announced it signed an agreement to acquire a substantial portion of Volta’s network, adding thousands of EV charging and digital media sites and formally entering the U.S. market. JOLT’s Volta agreement is framed as a step‑change: JOLT says it will add thousands of locations across the U.S., spanning up to 34 states and 64 DMAs. Industry reporting notes that final site counts can remain uncertain until close because both parties may still be coordinating with site hosts - an operational detail, not a legal footnote.

JOLT timeline

The central operating‑model question

JOLT is now attempting two compounding moves:

Accelerate AI‑enabled optimisation (higher change rate in data/decision loops).

Integrate and operate a much larger footprint with heterogeneous assets, site agreements, and potentially different operational norms.

The risk is not simply “integration complexity”. It is maturity interference: when Scale and Sense surge, the organisation often discovers its Stability and Systems controls were built for a smaller world.

These moves collectively imply a shift in operating model: Jolt is evolving from a network operated primarily as real estate + hardware, into a data‑and‑optimisation business where software updates and AI decision loops become core value drivers.

Let’s assess if JOLT’s operating system is capable of absorbing these two moves.

Stravus 8s Diagnostic Snapshot

Each dimension of the holistic 8S model is assessed using the Stravus maturity model (as explained here). Each S carries equal weight. Each one affects the others. It’s not about strength or ambition - it’s about maturity alignment. A company can operate at Innovator level in some domains and still be under strain due to unresolved gaps elsewhere. That’s where friction accumulates. And where even promising strategy can destabilise execution.

The Stravus 8S Digital Readiness Model (as explained here).

The Stravus maturity model (as explained here).

Below is JOLT’s diagnostic snapshot: what the public signals suggest about JOLT’s current structure and whether it puts it in a good place to tackle the two compounding moves at the same time.

JOLT - Stravus 8s Snapshot

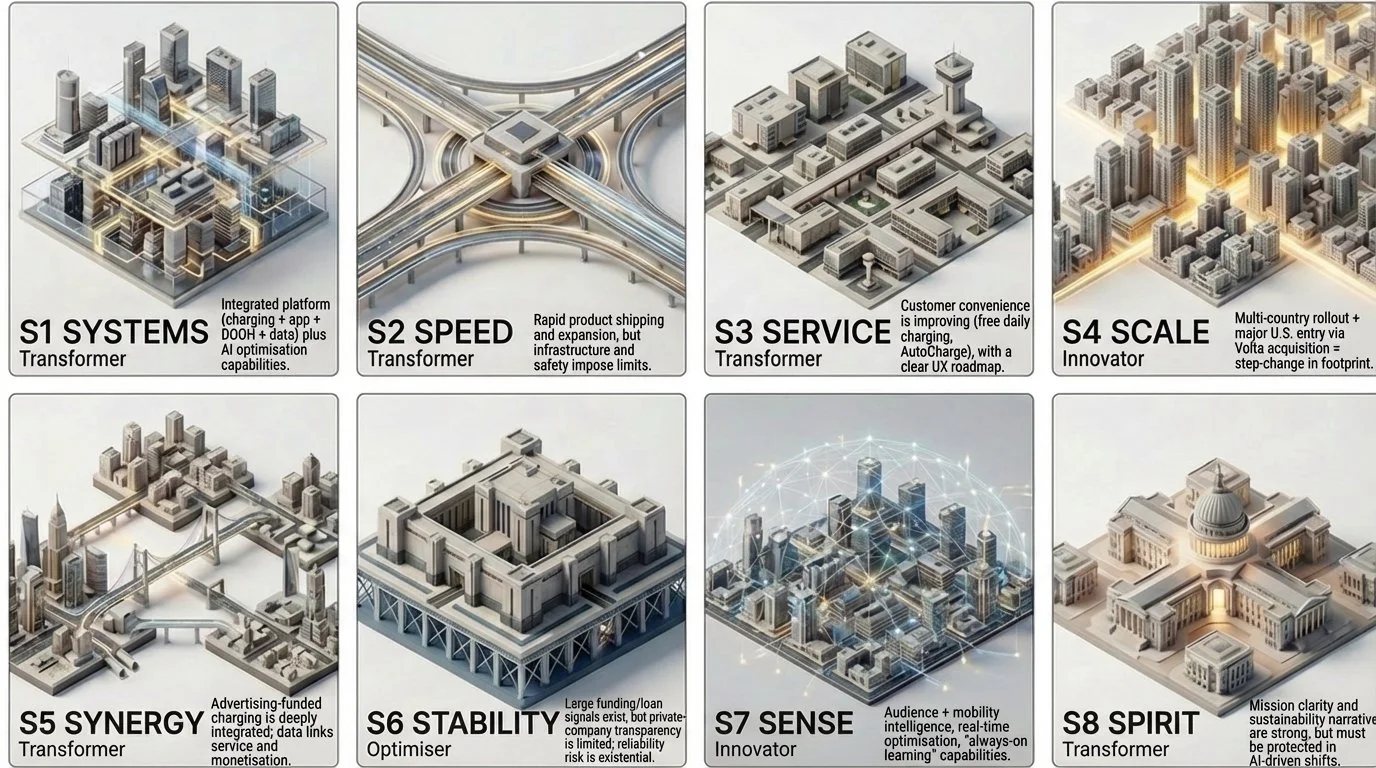

S1 Systems - Transformer

JOLT operates a composite system (chargers + screens + app + billing/entitlements + advertiser optimisation). Its Spark platform explicitly blends third‑party audience data with first‑party data and measurement tools, moving beyond “basic network ops” into a platform‑driven system. Systems remains Transformer (not Innovator) because the Volta agreement expands the technical and operational surface area across jurisdictions, site hosts and asset heterogeneity - requiring stronger integration patterns and lifecycle governance.

S2 Speed - Transformer

The release tempo is high: Spark launch (2024), AI optimisation augmentation (2025), AutoCharge (2025), next‑gen charger innovation (2025), plus the Volta U.S. expansion (2025). Speed is Transformer because EV infrastructure cannot safely run “software‑only” velocity without infrastructure‑grade controls; AEMO explicitly highlights “very high” risk scenarios from flawed EV charger software patches at system scale.

S3 Service - Transformer

Service design is explicit and evolving: free daily kWh (with service fee), app‑mediated support, and AutoCharge to remove session‑start friction. Service is Transformer because it is being actively engineered, not just delivered - but the public network is judged on “does it work now?”, not “is it online.” University evidence warns that uptime metrics can mislead and highlights failure modes such as payment issues and handshake failures.

S4 Scale - Innovator

JOLT demonstrates credible scale pathways: in Canada, it launched with plans to roll out 5,000 locations in partnership with TELUS. It also secured a Canada Infrastructure Bankpartnership (loan agreement) supporting up to 1,500 curbside fast charging ports, reinforcing the model’s financeability and deployment ambition. The Volta deal then creates a step‑change in U.S. footprint and advertiser reach.

S5 Synergy - Transformer

Synergy is JOLT’s core architecture: ad revenue subsidises charging; charging creates a high‑value engaged audience; Spark Intelligence converts that into measurable advertiser outcomes. Transformer is justified because synergy is designed into the model, but the Volta integration increases the coordination cost: the organisation must keep driver experience, advertiser optimisation, and site‑host requirements aligned across new U.S. operating conditions.

S6 Stability - Optimiser

Stability is supported by credible counterparties and long‑horizon partnerships (utilities, institutional capital, public finance). But Stability is best assessed through operational truth: reliability of charge initiation, payment/auth flows, and maintainability under change. Australian research argues “uptime” alone does not capture successful charging, and highlights real‑world failure modes. AEMO’s risk framing on software management underscores why Stability maturity must rise as the engineering change rate rises.

S7 Sense - Innovator

Spark Intelligence is explicitly Sense capability: real‑time analytics, attribution, audience mobility insight, and now AI‑driven real‑time optimisation with “always‑on learning.” This is Innovator maturity because it changes the decision loop - turning DOOH from a static broadcast asset into a continuously optimised performance channel (with measurable outcomes).

S8 Spirit - Transformer

JOLT consistently frames its mission as making it “faster, easier, and simpler” to switch to EVs, and positions itself as a “future‑facing public utility” (Spark Change). Awards (EV Startup of the Year; Best New Services) and recognition signals support legitimacy with councils and partners. JOLT also claims recognition by TIME and Statista (top 250 greentech companies), reinforcing brand proof‑points.

Overall maturity classification

Overall profile: High Transformer, with Innovator peaks in Scale (S4) and Sense (S7), and Optimiser‑level Stability (S6) as the constraint.

Imbalance pattern and the dual‑strategy tension: JOLT is attempting to compound the two most powerful (and most dangerous) accelerants at once:

Sense acceleration (AI optimisation and continuous decision loops).

Scale acceleration (U.S. entry via Volta + large‑partner rollouts).

When Sense and Scale surge together, there is typically one systemic risk: the change rate outgrows the organisation’s Stability envelope. In infrastructure, the “blast radius” of software errors is real - AEMO explicitly describes “very high” risk scenarios where flawed EV charger software patches cause serious system effects. Meanwhile, public evidence shows that user trust is built on successful charging, not “online” status, and failure modes often sit at the seams (payment, handshake, vandalism, blocked bays).

Opportunity: If JOLT successfully integrates Volta while maintaining reliability and upgrading release governance, AI‑enabled optimisation can improve advertiser ROI and raise subsidy capacity - reinforcing the flywheel and making global scale economically stronger.

Stravus recommended pathway

As explained in The Return of the Roaring 20s, we use the metaphor of a modern city to represent an organisation’s operating model. Each of the 8S dimensions is a critical district - interdependent, constantly in motion. Transformation is not a straight line; it requires deliberate movement across these interconnected domains. The Stravus pathway visual uses a metro map to illustrate that journey. The route isn’t arbitrary - it reflects a sequenced, system-level redesign. Each station matters. The order matters more.

Assumptions and data cut‑off: Public sources only; no internal operations, confidential metrics, or undisclosed integration plans. Data cut‑off 22 Feb 2026 (Australia/Sydney).

Sequenced pathway to make the dual strategy survivable

Stabilise first, integrate second, accelerate third is the wrong sequence for this model - because JOLT’s value is in motion.

The correct sequence is: Stability and Systems must rise in parallel with Integration and AI. This is an S6/S1 reinforcement programme that enables S4/S7 growth.

Quick Wins

Define and instrument “successful charging” as a first‑class KPI across both networks (JOLT + Volta).

Move beyond uptime into a metric set focused on successful session initiation and completion. This directly responds to the “uptime fallacy” problem highlighted by academic and industry analysis.

Expected outcome: reliability becomes measurable in a way that can be managed through integration.

Create a dual‑track release governance model (Infrastructure Core vs Optimisation Layer).

Treat charging initiation/payment/auth and charger control/firmware as “Infrastructure Core” with stricter gates; treat advertising optimisation as “Optimisation Layer” with feature flags, staged rollouts, and shadow mode testing. The rationale is simple: AEMO’s software‑management risk profile suggests low tolerance for uncontrolled change at infrastructure scale.

Expected outcome: Speed continues, but blast radius falls.

Run Spark AI optimisation in “shadow mode” during integration waves.

When integrating heterogeneous systems (site hosts, operational processes, asset estates), stabilise measurement first: run AI decisions in parallel and compare outcomes before activating at full scale. This approach retains innovation without destabilising integration.

Ring‑fence integration accountability.

JOLT notes that asset selection is “strategic” and the deal is conditional; reporting indicates site host discussions can affect final asset counts. Put one accountable operating leader over “integration reliability”, not just “integration close”.

Medium‑term moves

Build an “AI assurance layer” aligned to a recognised risk framework.

As Spark evolves into always‑on learning, implement formal evaluation/monitoring: drift, data integrity, unintended optimisation outcomes, and human accountability. NIST’s AI Risk Management Framework provides a practical lifecycle structure (govern/map/measure/manage) without prescribing a single implementation.

Expected outcome: Sense remains Innovator without eroding trust.

Adopt a secure SDLC baseline and automate it.

Higher change rates require stronger automated controls, not more meetings. NIST SP 800‑218 (SSDF) is a widely used secure‑development baseline that can be mapped into CI/CD gates (e.g., dependency hygiene, provenance artefacts, verification tasks).

Expected outcome: fewer production regressions; faster recovery; stronger governance for enterprise partners.

Standardise observability and incident response across geographies.

A key integration deliverable should be “one operational truth”: unified telemetry, unified incident taxonomy, consistent runbooks, and region‑based rollback capability. This is where Systems maturity moves from Transformer toward Innovator.

Illustrative QA controls table

Data cut‑off is 20 February 2026 (Australia/Sydney). This diagnostic uses public information only (press releases, filings, credible press); it does not include internal operating metrics, confidential integration plans, or non‑public regulatory correspondence.

Investor/owner verdict

Based on public evidence, the dual strategy is sensible, but conditionally risky.

Sensible because JOLT’s Sense advantage (Spark + AI optimisation) is directly monetisable, and U.S. Scale via Volta dramatically expands inventory and advertiser reach - exactly where the flywheel compounds.

Risky if Stability remains Optimiser while Scale and Sense surge. Infrastructure businesses do not get to “move fast and fix later” when failures are physical and reputational - AEMO’s “very high” software‑management risk framing is the technical reflection of that business fact.

Prioritised sources

Primary / official

JOLT Australia: core proposition (7kWh free daily, GreenPower).

JOLT Support: service fee and charging mechanics (AU/NZ).

JOLT: Spark Intelligence launch (audience analytics, impression‑based approach, 18m users).

JOLT: Spark Intelligence AI real‑time optimisation enhancement (always‑on learning).

JOLT: AutoCharge release (plug‑and‑go).

JOLT: Volta acquisition agreement (scope, close date, U.S. footprint).

Austroads + ARENA: Adelaide trial and ad‑funded model documentation.

Canada Infrastructure Bank project page: 1,500 curbside ports and model summary.

Australian / credible analysis on risk and reliability

University of Queensland analysis: uptime vs real usability; handshake/payment failure modes.

Australian Energy Market Operator (AEMO) report: “very high” risk scenarios for EVSE software management failures.

Governance and QA baselines

NIST AI RMF 1.0 (trustworthy AI risk lifecycle).

NIST SP 800‑218 SSDF (secure software development baseline).