Gold versus Bitcoin: A Stravus Operating System Analysis

Executive Summary

In early 2026, gold and Bitcoin – both touted as reserve assets – are diverging: gold prices are hitting new highs on geopolitical uncertainty while Bitcoin is in a mid-cycle drawdown. An “operating-system” (OS) lens (Stravus 8S framework) helps cut through price noise by analysing each as a system with architecture, processes and culture. Gold’s Systems and Stability remain strong – it is deeply embedded in central bank operations and crisis-hedge lore – whereas Bitcoin leads on Speed and Spirit (decentralisation, innovation). Mapping each S reveals gold as a mature “Optimiser” asset (stable, institutionalized) and Bitcoin as a fast-evolving “Transformer” (gaining robustness but still maturing). The table below summarizes key 8S metrics, with illustrative 1–10 scores (higher = more developed):

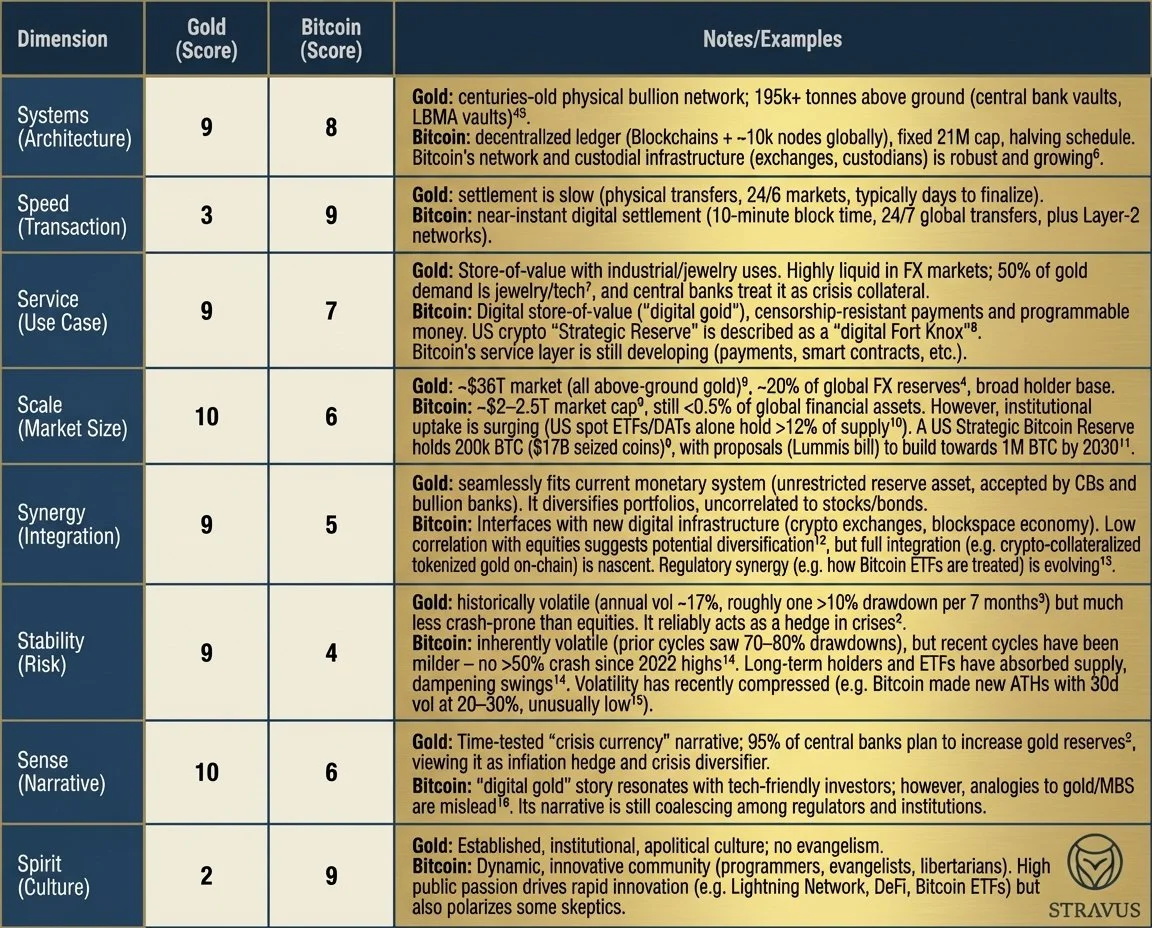

Gold versus Bitcoin comparison table

Using these scores, Gold stands out in traditional reserve metrics (Systems, Service, Stability, Sense) and rates as an Optimiser-stage asset: time-tested, reliable, with incremental improvements (e.g. digitisation of vaulting, more ETF integration). Bitcoin scores higher on Speed and Spirit, reflecting cutting-edge capabilities, and is best viewed as a Transformer: it has transitioned from a niche Survivor (early days) into a substantial Transformer stage, where rapid innovation and institutional adoption are reshaping its role. If current trends continue (volatility moderating, regulatory clarity improving), Bitcoin could approach Innovator status by 2030 – coexisting with gold as a recognised reserve (as Deutsche Bank strategists suggest).

Stravus 8s Diagnostic Snapshot

An operating-model (OS) lens treats each asset as a complex system (like a firm) rather than just a price series. Stravus’s 8S framework (as explained here) examines Systems, Speed, Service, Scale, Synergy, Stability, Sense, Spirit.

This reveals non-price factors critical for a reserve asset. For example, gold’s Systems include physical mines, refinery processes and vault infrastructure; Bitcoin’s includes its cryptographic protocol and global node network. The OS view highlights structural strengths and gaps. As Wharton professors note, analogies (e.g. “Bitcoin = gold”) can mask deep differences: Bitcoin lacks gold’s tangible value and transparent quality. An OS analysis forces us to ask: does Bitcoin have (or need) the same institutional underpinnings as gold (e.g. trusted custodians, clear valuation)?

This lens is useful because central banks and institutions care about architecture: liquidity, risk, governance, and integration. For instance, US policymakers have begun treating Bitcoin as part of systemic policy – an executive order created a U.S. “Strategic Bitcoin Reserve” of seized coins, explicitly calling the stored BTC a “store of value” akin to a digital Fort Knox. That policy move underscores how Bitcoin’s systems (custody, regulation) and sense (official recognition) are evolving. By contrast, gold’s operating model is well-known: stable supply/demand, central bank protocols, and decades of market microstructure. This means gold’s operating model rating is high, while Bitcoin’s is improving from early-adopter survival mode.

Mapping 8S thus provides an evidence-based comparison across multiple dimensions. Below we analyse each S for Bitcoin vs. gold, citing primary data and expert reports where available.

S1 Systems

Gold: Established physical network. Global gold reserves (~195k tonnes) reside mainly in mint-held bars and commercial vaults; mining adds only ~3,000t/year. Central banks widely use GLD/Vault systems and LBMA market makers. According to JPMorgan/World Gold Council, developed-market central banks hold ~46.5% of their reserves in gold (3Q 2025), reflecting deep institutional reliance. Gold’s ownership and quality verification are transparent via assays.

Bitcoin: Digital ledger platform. Bitcoin’s system is open-source code running thousands of nodes; issuance is algorithmic (21M cap, halvings). Its “custody chain” relies on crypto exchanges, custodians and hardware wallets. The institutional-grade infrastructure has strengthened: by end-2025, Bitcoin spot ETF and Digital Asset Treasury (DAT) programs held >12% of BTC supply, and major banks (e.g. Morgan Stanley, Vanguard) began offering crypto custody products. A U.S. “Strategic Bitcoin Reserve” is being built from seized coins (~200k BTC) (with plans to possibly add more via Treasury programs). As ARK notes, Bitcoin is becoming a “globally traded macro instrument” supported by robust trading, liquidity, and custodial infrastructure.

S2 Speed

Gold: Slow. Physical gold trades on weekday markets, with settlement typically 2–5 days (swaps, deliveries). Vault transfers and shipping can take weeks.

Bitcoin: Fast. Block confirmations occur ~every 10 minutes (speeding up with off-chain networks). Settlement finality is near-instant (no trading “hours” – 24/7 market). In practice, BTC can move value worldwide within an hour, much faster than moving bullion. This gives Bitcoin an OS advantage in agility.

S3 Service

Gold: Multipurpose store-of-value. Gold serves as central bank collateral and a commodity. Roughly half of annual demand is industrial/jewelry use. It pays no yield but is trusted for crises: CBs cite “performance in crisis, store of value, diversifier” as reasons to buy more. Gold refiners, ETFs (GLD, etc.) and futures (COMEX, etc.) support service needs. Its value structure is tangible: purity tests are straightforward, and it has a long track record of value preservation through wars and inflation..

Bitcoin: Purely digital store-of-value (and settlement layer). It offers programmability (smart contracts, Lightning payments) that gold cannot. Service tasks include censorship-resistant remittances and on-chain collateral. The US crypto czar analogized the Bitcoin Reserve to “digital Fort Knox” for a currency called “digital gold”. However, Bitcoin’s “diversifier” role is less proven. It has no physical utility and its value depends on confidence in the network. To date, Bitcoin has not been stress-tested in a fiat collapse; its ability to serve (e.g. transact during grid failures) is unproven.

S4 Scale

Gold: Largest non-sovereign market. Estimates place total above-ground gold at ~$36–37T. Gold is deeply embedded in portfolios: global official sector holds ~35k+ tonnes (≈$2.2T). The market is liquid: the London market handles ~$150B+ daily. Central bank buying has surged (>1,000t/yr since 2022) as CBs diversify away from dollars. Total retail and ETF investment also doubled in recent years.

Bitcoin: Still much smaller. Market cap is ~$2–2.5T (Bitcoin alone), versus ~$25–30T in gold. In absolute terms, this is tiny relative to global reserves or other asset classes. However, growth is rapid: by early 2026, SEC-approved spot ETFs and corporate treasuries hold billions. For example, corporate “Digital Asset Treasuries” (DATs) like Strategy hold ~1.1M BTC (~5.7% of supply, ~$90B). The U.S. Treasury’s fledgling Bitcoin Reserve already commands ~200k BTC. ETFs and regulated vehicles are absorbing new issuance (mining) at unprecedented rates. So relative growth in scale has been dramatic, but absolute size remains modest. This gap underscores why Bitcoin can only augment, not replace, gold’s scale – at least over the next few years.

S5 Synergy

Gold: High synergy with current system. Gold dovetails with existing monetary frameworks. It remains a core “currency alternative” for central banks – as one CB survey noted, 73% expect global gold share of reserves to rise as USD share falls. Portfolio managers use gold for diversification (gold’s correlation with stocks/bonds is low). Importantly, gold’s ecosystem (vaults, ETFs, OTC market) plugs straight into financial plumbing with no new regulatory paradigm required.

Bitcoin: Partial synergy via new rails. Bitcoin adds digital age features: 24/7 liquidity, easy divisibility, auditable scarcity. It can complement FX reserves in a tokenized future, but currently requires new infrastructure (crypto exchanges, interoperable blockchains). Some synergy exists: stablecoin systems use Bitcoin as backing; banking-level ETFs tie Bitcoin to traditional accounts. Yet Bitcoin still lacks the universal acceptability gold has. Regulatory frameworks (e.g. US “Clarity Act” proposals) are only now catching up. Bitcoin’s synergy will grow if on-ramps (custody, integration with payment systems, clear laws) improve.

S6 Stability

Gold: Historically resilient. Over 20 years, gold’s annualized volatility ~17% (slightly above equities), but it has never crashed 80–90% (unlike stocks or Bitcoin). Major corrections do occur (~10–20%), but these are short-lived. For institutions, gold is a known risk profile: one study found gold outperformed in 6 of the last 5 crises, averaging +6% when S&P fell 20%. Even during Fed tightening, gold has held near-record levels. That said, gold is not immune to drawdowns; JPMorgan notes 91 drawdowns >10% since 1975 (~one every 7 months).

Bitcoin: Still volatile but settling. Bitcoin’s infamous 60–80% crashes have eased: ARK Invest notes no >50% peak-to-trough drops in the latest cycle, suggesting deeper liquidity. Recent multi-day stability (Bitcoin closed above $100K for 53 days in a row in mid-2025) hints at greater resilience. However, Bitcoin remains far riskier: policy shifts or large sell-offs can still swing price by >10% in a day. Critics emphasize this: a Reuters legal piece warned Bitcoin “remains too young and volatile” with security risks for reserves. Institutions view Bitcoin as “almost” a reserve asset but acknowledge its current volatility gap.

S7 Sense

Gold: Crystal-clear narrative. Gold’s role is intuitively “the crisis hedge.” It has centuries of precedent. According to the World Gold Council’s 2025 survey, 95% of central bankers believe global gold reserves will rise in the next 12 months. Gold is widely perceived as inflation-resistant and a diversifier of fiat risk. There is virtually no debate over gold’s store-of-value function (unlike stocks or crypto).

Bitcoin: Emerging narrative. Many (from tech CEOs to punters) champion Bitcoin as “digital gold” – a modern, high-velocity store-of-value that survives any fiat upheaval. This narrative drove Bitcoin’s massive gains and adoption (e.g. El Salvador’s legal-tender experiment). However, experts caution that such analogies can be misleading. Wharton professors note that comparing Bitcoin to gold can obscure Bitcoin’s opaque ownership and extreme speculation. Unlike gold, Bitcoin has no intrinsic industrial value and its supply is unbacked outside consensus. Thus, while Bitcoin’s “scarcity narrative” is potent, it lags gold’s old and convincing story. We see this in markets: gold rallying on real-world shocks, while Bitcoin sometimes responds in reverse or later (e.g. gold led bitcoin in past cycles).

S8 Spirit

Gold: Traditional. Gold’s culture is conservative and institutional. There is no community hype; gold moves on economic fundamentals and central bank mandates. It neither has nor needs a vibrant “community.”

Bitcoin: Revolutionary. Bitcoin’s spirit is populist, technocratic, and anarchic. Its community values decentralization, permissionless innovation and distrust of central authority. This energy has pushed rapid development (e.g. Lightning Network scaling, decentralized finance). It also attracts political interest – the US Bitcoin Reserve order and blockchain bills show how political “tribes” (fiskal hawks vs crypto-libertarians) view it. The intensity of this culture can be a double-edged sword: it accelerates growth but also polarizes opinion (some see Bitcoin as too ideological or risky).

Diagnostic Scoring and Maturity

The diagnostic table above suggests Gold is highly rated in Stability, Sense, Systems, etc., while Bitcoin scores especially on Speed and Spirit. These scores (1–10) are illustrative, based on qualitative and quantitative indicators (central bank surveys, market data, volatility, adoption metrics). Stravus uses a maturity model (as explained here) to assess the overal maturity based on the 8S diagnostic:

Gold – Optimiser: It is a mature reserve asset, well-understood by institutions. Its operating model is optimised for stability and scale, with incremental technical improvements (e.g. more ETF access, digital bullion). Gold’s 8S profile is “Optimiser”: steady, reliable, with room for efficiency gains (better logistics, partial tokenisation).

Bitcoin – Transformer: Bitcoin’s profile fits a “Transformer”: it has moved beyond a mere experiment into an asset transforming institutional behaviour. It still has higher risk and unknowns (regulatory, technological), so it’s not yet “innovator”-stage. But compared to 10 years ago, it has made the leap into serious consideration. If trends continue (growing infrastructure, reduced volatility), Bitcoin could approach Innovator status as it carves out a new niche (analysing digital reserves).

Short-Term vs Long-Term Pathways

Short-Term (0–4 quarters): The current divergence likely persists. With inflation fears and geopolitical risk high, gold’s established safe-haven status will keep demand strong. Central banks and wary investors will add gold. Bitcoin, by contrast, will remain sensitive to market sentiment. The Feb 2026 sell-off (triggered by system events and risk-off cues) was an example of Bitcoin’s reliance on broad risk appetites. Price aside, Bitcoin’s underlying demand sources (ETFs, corporate treasuries, SBR) are steady, but the volatility regime is tighter – large, sudden swings seem smaller now. Short-term watchers should note that Bitcoin’s biggest drawdowns may now come from “funding shocks” (ETF liquidations, margin calls) rather than fundamental collapses. In any case, an OS view suggests gold’s Systems and Stability give it immediate resilience, whereas Bitcoin’s Service and Spirit are still proving themselves.

Long-Term (1–5 years+): Over multiple years, a new equilibrium may emerge. Many analysts (DB, Ark, Bitwise) foresee both assets rising in tandem as “hard” assets. Key drivers will be inflation dynamics, monetary policy, and technological adoption. Gold’s inflation-hedge rationale should remain intact – demand from Asia (China/India) and diversification away from the dollar is likely. Bitcoin’s upside will depend on continued institutional integration. For example, if macro conditions (lower real rates, easier Fed policy) revive risk appetite, Bitcoin could “catch up” to gold’s gains (as Bitwise argues, precious metals might lead and Bitcoin follow). By 2030, central banks may allocate to both: DB projects co-existence of Bitcoin alongside gold on reserves. In that scenario, Bitcoin would have progressed from a specialized innovation to a recognized macro asset. Its Scale and Stability would need to narrow gaps (e.g. one study suggests if Bitcoin’s volatility falls further, it could improve portfolio Sharpe ratios due to low correlation).

Watchlist: Maturation Signals

Which signals would indicate Bitcoin is maturing toward a bona fide reserve asset? Key metrics to monitor over coming quarters and years:

Volatility Regime: Look for sustained low volatility at high price levels. For instance, Bitcoin’s 53-day streak above $100K in mid-2025 was noted by Fidelity as a maturity signal. Similarly, realize volatility remaining in the low 20–30% range even as price rises would signal institutional stability. If Bitcoin can hit new highs without wild swings (unlike past cycles), that suggests deeper liquidity and confidence.

Institutional Flows & Holdings: Continued large net inflows to crypto ETFs, corporate treasuries, and sovereign reserves. Kraken notes 2024–25 saw ~$44B net spot demand from US ETFs and public DAT firms. Watching ETF AUM growth, new institutional products (like bond or yield products on Bitcoin), and balance sheet allocations (e.g. U.S. states or foreign CBs disclosing BTC holdings) will show if institutional demand is structural. If major banks (beyond custody) actually invest their own treasuries, that’s another sign.

Policy and Regulation: Progress on clarity (e.g. passage of the US CLARITY Act on digital commodities, clarity from world’s big CBs) would reduce uncertainty. Key indicators include: new official reserve programs (other countries setting up Bitcoin reserves after US did), tax/treaty changes, and global regulatory alignment. For example, a decision by the IMF or BIS to study or accept Bitcoin as “crypto asset reserves” would be a watershed. Also, stablecoin legislation (bolstering on-chain dollar liquidity) indirectly supports Bitcoin’s ecosystem.

On-Chain and Network Metrics: Increased on-chain activity by long-term holders (higher “coin days destroyed”), implying the market is digesting new supply. Ark noted record Coin Days Destroyed in 4Q25 – showing some legacy holders finally selling. Watch for this to normalize. Also watch Lightning Network growth and daily transaction volumes. Improvement in such usage metrics suggests Bitcoin is being used more like money (service) rather than speculative token.

Correlation Behavior: If Bitcoin’s correlation with gold (or other safe-havens) starts to rise during downturns, it may be acting more like a crisis hedge. Currently the BTC–gold correlation is low; a trend toward positive or less negative correlation in risk-off periods would hint at maturing “digital gold” role.

Benchmark Indicators: Break-even inflation rates, dollar index (DXY) – since Bitcoin is partly driven by fiat debasement narratives. If Bitcoin consistently rallies while real yields rise (i.e., like gold did in 2025), it might confirm its anti-fiat role is accepted. Conversely, if Bitcoin underperforms when yields spike, that’s a warning.

Market Depth & Liquidity: Measures like order book depth on major exchanges, futures open interest, and funding rates staying benign (low chance of squeezes). This is harder to quantify, but exchange data (e.g. open interest/OI vs. realized volumes) could indicate if Bitcoin can absorb big trades without shocks.

Each signal should be interpreted in context. For instance, a flat price could be bullish (stability in the face of external shocks) or bearish (loss of interest). Thus, institutions should track a basket of signals rather than price alone.

Strategic Takeaways for Institutions

Maintain Gold for Stability: Gold remains the archetypal reserve asset. Its long-held role, physical scarcity and portfolio diversification benefits are undiminished. Institutions should continue core allocations to gold to hedge against inflation and crises (as central banks overwhelmingly plan). Even as Bitcoin matures, gold’s extensive liquidity and familiarity make it the anchor in any reserve mix. Consider leveraging the current rally (record highs) to rebalance or secure gains, since gold’s high in 2026 reflects strong fundamental demand (geopolitical risk, CB buying).

Build Crypto Infrastructure and Governance: If Bitcoin is to be treated as a quasi-reserve, the operating environment must be up to institutional standards. This means investing in secure custody (insured custodians, multisig policies), compliance frameworks, and risk management for crypto (cybersecurity, stablecoin usage). The OS analysis shows Bitcoin’s Systems and Stability need institutional-grade reliability. Institutions should pilot and expand regulated crypto products (like spot ETFs, stablecoin settlement) in parallel with gold. Monitoring legal developments (e.g. crypto legislation) is crucial. For example, the US Strategic Bitcoin Reserve order is largely symbolic now, but full legalization or central bank involvement would drastically change the landscape. Institutions should be ready – e.g. by performing due diligence on Bitcoin custody providers or stress-testing digital asset liquidity just as they do for gold.

Adopt a Diversified Reserve Mindset: Ultimately, Bitcoin and gold need not be “either/or.” Each excels under different conditions. The OS view suggests gold remains king under acute uncertainty (its Stability and Sense are unmatched), whereas Bitcoin offers a high-growth, high-speed counterweight (Speed, Spirit). Strategic reserve policy should leverage both: gold for baseline stability, Bitcoin for upside participation in a digital economy. As Kraken notes, regulatory clarity is tilting in favor of crypto, and DB Research even foresees co-holding by 2030. Institutions should define clear allocation frameworks: e.g. small, fixed Bitcoin positions that grow with maturity, rather than large speculative bets. Finally, watch those OS signals. If Bitcoin begins to tick off maturation checkboxes (sustained price/vol stability, broader adoption), incremental reserve allocations may be justified. In all cases, risk management (hedging, liquidity buffers) should mirror gold’s, adapting to Bitcoin’s unique volatility and operational risks.

In summary, an 8S operating-model analysis shows gold is currently the more proven reserve asset (an Optimiser on all counts), while Bitcoin is an accelerating challenger (a Transformer trending toward Innovator). Short-term, allocate according to these structural strengths. Long-term, prepare infrastructure and keep watchful for the maturation signals that would elevate Bitcoin’s role alongside gold. Both assets appear likely to co-exist as part of a diversified institutional reserve strategy – the former as a bedrock store-of-value, the latter as a next-generation digital reserve.

Sources: Reuters, Bloomberg and industry reports on gold and Bitcoin; academic analyses; and crypto/finance research. These inform the comparative analysis above.