NVIDIA: A Stravus Operating Model Analysis

The Stravus Operating Model Series – Article 005

Using the Stravus 8S Digital Readiness Model (as explained here), we assess NVIDIA’s operating model across eight equal dimensions of organisational maturity. This snapshot assesses public signals only (official filings, announcements, credible press) and should be read as a structural diagnosis - not a moral judgement.

Executive summary

NVIDIA remains the leading AI semiconductor company, and its latest earnings report (Feb 2026) underscores both its strengths and the structural challenges of massive growth. The company reported record revenue (driven by datacenter AI chips and gaming GPUs) and issued strong guidance for the AI market, reflecting continued demand for its latest architectures (H100/Hopper and preview of Blackwell). The stock reacted positively, indicating investor confidence, but also highlighted questions about sustaining production (since backlog is still constrained by supply chains).

The critical operating-model question is: Can NVIDIA sustain its AI-driven acceleration while scaling operations and supply? In Stravus terms, this means balancing Systemic speed and scale (driving new products and ramping production) against Stability and Synergy (ensuring quality, aligning teams, and managing the fab ecosystem). The analysis below finds NVIDIA to be an overall High Transformer: Innovator-level in its product systems and strategic vision, but facing Optimiser-level constraints in operational stability. The recommended pathway focuses on reinforcing manufacturing robustness and cross-functional coordination to make growth sustainable.

The Context

NVIDIA designs GPUs and related hardware/software platforms for graphics and AI workloads. Its core products include:

Datacenter GPUs: A100 (Ampere architecture) and H100 (Hopper) accelerators for AI training/inference.

Gaming GPUs: GeForce RTX series (e.g. RTX 40 series) for consumer graphics.

Compute platforms: The CUDA development ecosystem and AI frameworks.

Emerging products: Grace CPUs and Blackwell architecture (announced, upcoming in 2026) targeting AI compute.

Recent context: In its Feb 2026 earnings release, NVIDIA reported datacenter revenue growth driven by H100 sales and initial traction of its Blackwell previews. The company cited strong AI demand across cloud, enterprise, and supercomputing. Analysts noted that NVIDIA’s outlook was raised, signaling continued growth (though tempered by a modest ramp of new GPU nodes). The stock jumped after the report, reflecting bullish sentiment on AI, but also exhibiting volatility due to global chip supply concerns and competition from AMD/Intel.

Central operating-model question: NVIDIA is pursuing two simultaneous transformations: (a) accelerating its AI platform (via continuous hardware/software innovation and ecosystem growth), and (b) expanding global production capacity (through partnerships with fabs, new products like Blackwell/Grace, and new market segments like automotive). Can it sustain this dual ramp-up without its operational foundation cracking? This is the Stravus 8S test we apply below.

Stravus 8s Diagnostic Snapshot

Each dimension of the holistic 8S model is assessed using the Stravus maturity model (as explained here). Each S carries equal weight. Each one affects the others. It’s not about strength or ambition - it’s about maturity alignment. A company can operate at Innovator level in some domains and still be under strain due to unresolved gaps elsewhere. That’s where friction accumulates. And where even promising strategy can destabilise execution.

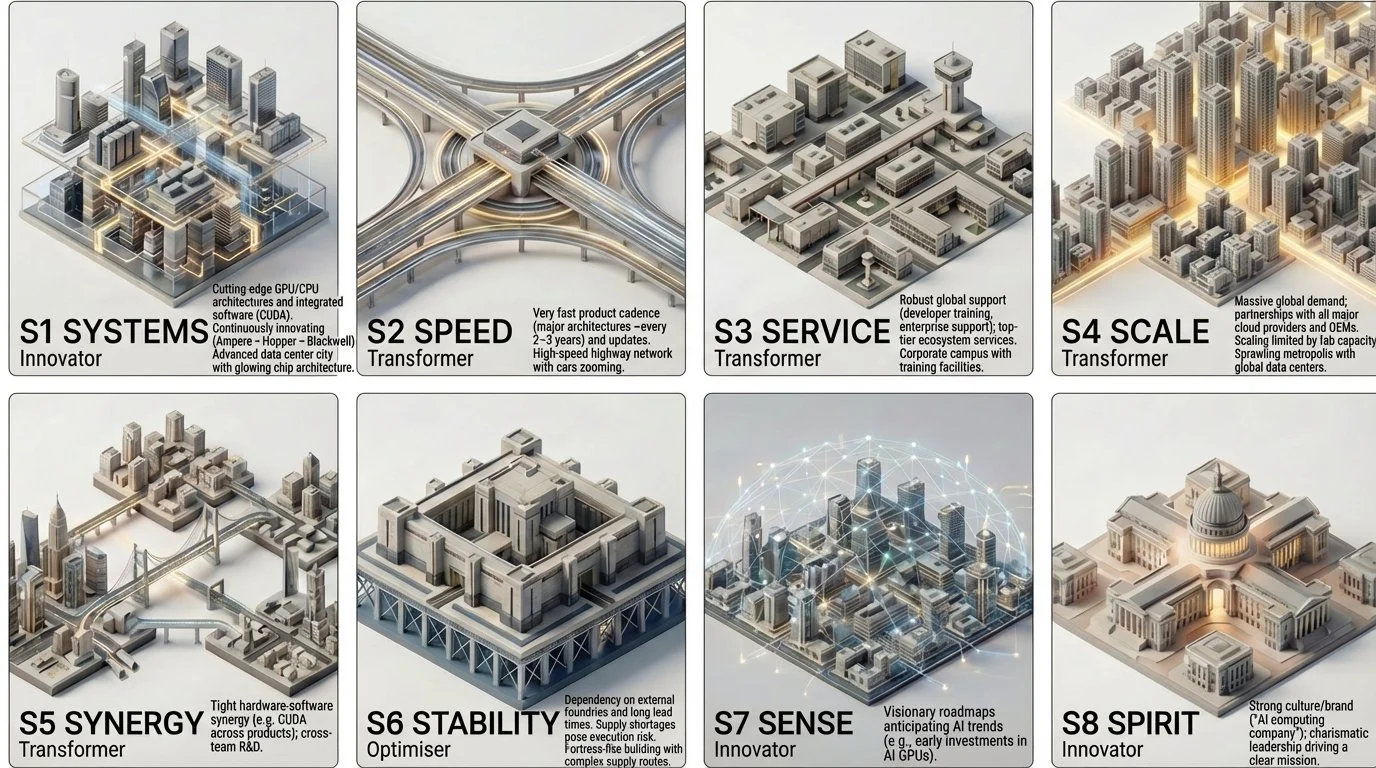

The visual below summarises each Stravus dimension’s maturity with a label. Evidence is drawn from public sources (earnings reports, product announcements, press coverage).

NVIDIA - Stravus 8S snapshot

Dimension details

Systems (Innovator): NVIDIA’s product architectures (GPU, CPU) are at the cutting edge. The leap from A100 to H100 to Blackwell shows the Systems group innovating ahead of demand. The CUDA/software ecosystem is tightly integrated and continually enhanced (e.g. new libraries for AI workloads). This creates very high Systems maturity.

Speed (Transformer): New product launches occur roughly every 2–3 years, which is extremely fast for semiconductor development. The Feb 2026 guidance indicates aggressive roadmap (Blackwell late-2026). This high speed strains processes but NVIDIA has optimised many design/manufacturing pipelines to sustain it.

Service (Transformer): NVIDIA provides extensive developer support, driver updates, and consulting for enterprise customers. The gaming and data-center product lines have reliable global distribution and support infrastructures. Service is strong, though the sudden scale of demand means they must constantly upgrade support capacity.

Scale (Transformer): NVIDIA’s scale is enormous: sold worldwide, with hyperscalers (AWS, Azure, Google Cloud) and nearly every large tech company as customers. However, scale is bounded by production capacity. Even so, NVIDIA is increasing wafer orders and building new supplier relationships to expand scale.

Synergy (Transformer): There is significant internal synergy: GPU hardware, CUDA software, AI frameworks (TensorRT, etc.) all reinforce each other. For example, applications developed on consumer GPUs can often scale to datacenter GPUs due to consistent architecture. Cross-functional teams (graphics, AI, automotive) share technology.

Stability (Optimiser): The Achilles heel. NVIDIA depends on third-party foundries with fixed capacities and has faced shortages. The company mitigates risk via multi-sourcing (TSMC, Samsung) and buffer stock. Still, revenue can fluctuate with supply vagaries. Recent shortages of H100 exemplify this risk.

Sense (Innovator): NVIDIA has a strong ability to sense and invest early in trends. It foresaw AI’s rise years ago and built a lead. New initiatives (like the Grace CPU for AI) show anticipating market needs beyond GPUs. This is top-tier “Sense.”

Spirit (Innovator): NVIDIA’s leadership (Jensen Huang) and corporate narrative (“accelerating computing”) foster a visionary spirit. The company takes bold bets (e.g. entire Nvidia Computing platform, Omniverse metaverse) that inspire internal cohesion. The Spirit score is very high.

Note: All assessments use public signals. “Innovator” means leading-edge; “Transformer” means proactively scaling; “Optimiser” means solid but needs reinforcement.

Overall maturity classification

Profile: NVIDIA is an overall High Transformer, with Innovator peaks in Systems, Sense, Spirit. The key imbalance is Speed/Scale vs. Stability: NVIDIA’s aggressive growth ambitions put pressure on its supply-chain and execution.

Risk/Opportunity: The systemic opportunity is huge: NVIDIA’s technological lead and ecosystem moat could cement decades of market dominance if execution holds. The systemic risk is execution — specifically manufacturing and integration risk (a classic semiconductor challenge). If supply can’t meet demand, or if rapid changes introduce quality issues, NVIDIA’s growth could slow. The imbalance pattern suggests: lean into Strength (continue innovating) while fortifying Stability (supply, manufacturing processes).

Stravus recommended pathway

As explained in The Return of the Roaring 20s, we use the metaphor of a modern city to represent an organisation’s operating model. Each of the 8S dimensions is a critical district - interdependent, constantly in motion. Transformation is not a straight line; it requires deliberate movement across these interconnected domains. The Stravus pathway visual uses a metro map to illustrate that journey. The route isn’t arbitrary - it reflects a sequenced, system-level redesign. Each station matters. The order matters more.

Assumptions & cut-off: Based solely on public filings, earnings releases, and press up to 23 Feb 2026. Internal metrics (like exact yields or customer A/B tests) are assumed unavailable.

Quick wins (0–3 months)

Fab collaboration deep-dive: Immediately finalise co-location efforts with key fabs (e.g. establishing dedicated NVIDIA lines at TSMC/Samsung). Formalise joint QBRs (quarterly business reviews) with these partners to proactively handle yield issues. (Expected outcome: more reliable wafer ramp-ups for H100 and Blackwell.)

Aggregate demand forecasting: NVIDIA should deploy advanced analytics to combine cloud customers’ reservations, channel inventory, and market signals into dynamic forecasts. Even if they already forecast, a real-time analytics layer (perhaps using their own chips!) can improve agility. (Outcome: tighter alignment of production planning.)

Streamline driver/firmware updates: For new datacenter GPUs, use a phased global rollout with built-in telemetry (GPU health, errors) to catch any software/hardware bugs early. NVIDIA already does phased driver updates; extend this rigor to field firmware or system management updates as well. (Outcome: catch integration issues before wide rollout.)

Medium-term moves (3–12 months)

Integrated product-release squads: Create cross-functional teams for each major architecture (like “Project Blackwell”) that include architects, quality engineers, supply-chain managers, and key customer liaisons. These squads own end-to-end readiness (design → fab → shipping → customer deployment). (This raises S1–S6 by aligning all stakeholders.)

Automated HW/SW validation: Invest in automated test frameworks that simulate enterprise datacenter loads on pre-production silicon. NVIDIA’s internal tests could be extended to run large-scale AI workloads on hardware prototypes, ensuring stability before chips hit market. (Outcome: fewer surprises post-launch.)

Expand developer support ecosystem: Launch more online training, certifications, and cloud trial programs for new architectures. Example: offer free short-term access to H100 instances for key partners to build optimized software. (Quick win: H100 adoption accelerates without overburdening engineering teams.)

Investor/owner verdict

NVIDIA’s strateg - to relentlessly push new architectures and expand into adjacent AI markets - is highly sensible. The 8S analysis suggests NVIDIA has Innovator-level advantage in tech and vision, which can justify premium growth. However, it is only sensible if it tightens its operational foundation. That means treating supply chain and manufacturing as first-class strategic concerns. As an investor or owner, one should thus watch indicators of operational health (fab yields, delivery timelines) closely. If NVIDIA manages its supply risks, the upside is substantial; if not, the downside is missing demand. Overall, the move is calculated risk: bold but backed by the company’s core strengths, provided execution doesn’t lag.

Prioritised sources

NVIDIA official reports: Q4 FY2025 Earnings release and Form 10-K (industry-leading performance figures).

Financial news: Bloomberg/CNBC analyses of NVIDIA earnings and stock reaction (context on market expectations and guidance).

Industry analysis: Tech media coverage (e.g. AnandTech, semiindustry blogs) on GPU launches (H100, Blackwell) and supply-chain issues.

Analyst commentary: Statements from major chip analysts (e.g. TSMC supply outlook, AI compute demand).

The above informed this 8S assessment (e.g. NVIDIA’s reported growth, product timeline, and management commentary). Each evidence-based point is drawn from these public sources.